Amazon’s dominance of online retail means that hundreds of thousands of small businesses must rely on its site to reach customers. In this report, we find that Amazon is exploiting its gatekeeper power to extract a growing cut of the revenue earned by these sellers. It’s doing this by imposing ever-larger fees on them. This tactic is hobbling sellers and often dooming their businesses. It’s also enabling Amazon to entrench its monopoly grip on e-commerce, while expanding its dominance into logistics and advertising.

Key Findings:

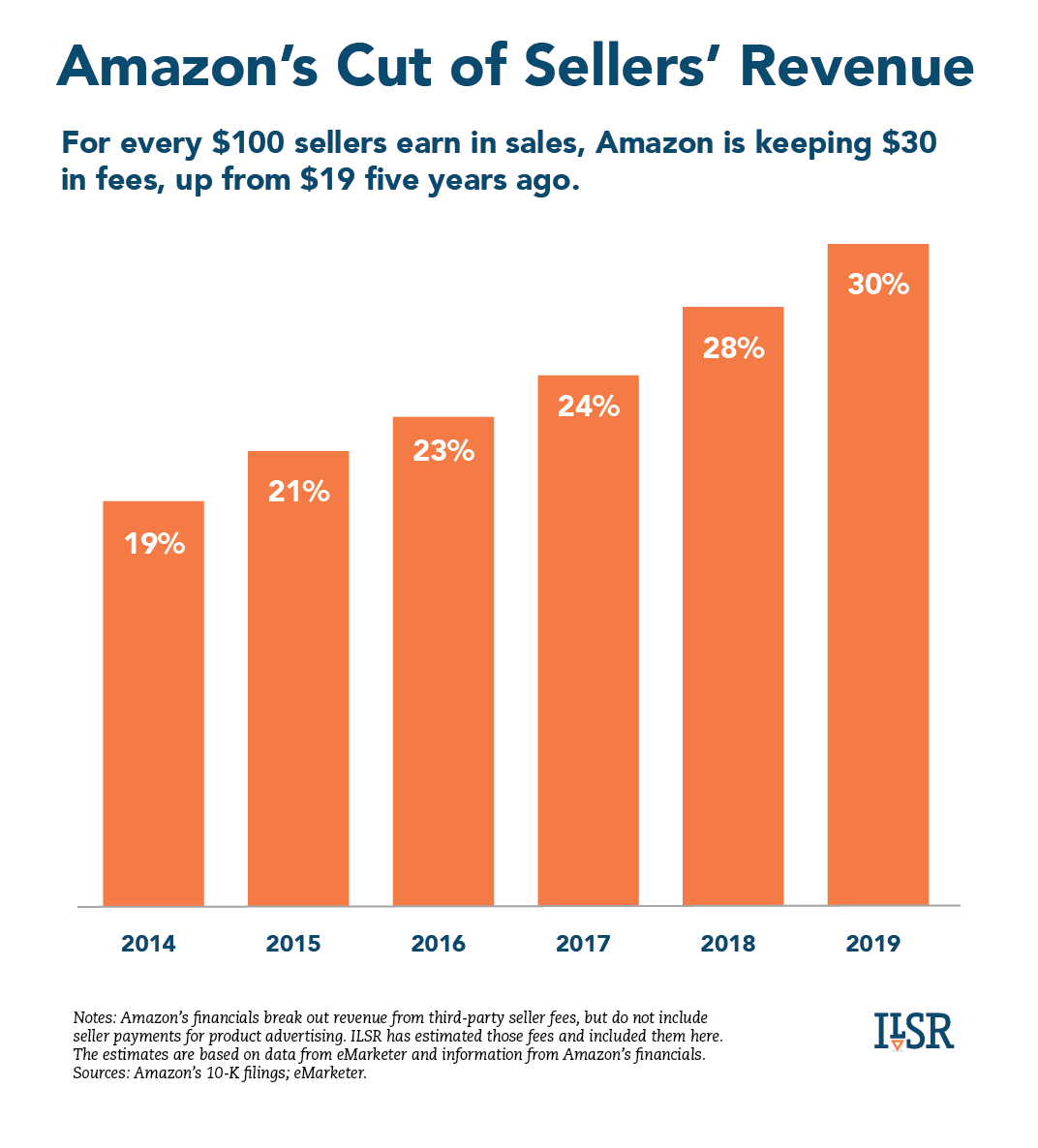

- Amazon keeps an average of 30 percent of each sale made by independent sellers on its site, up from 19 percent just five years ago.

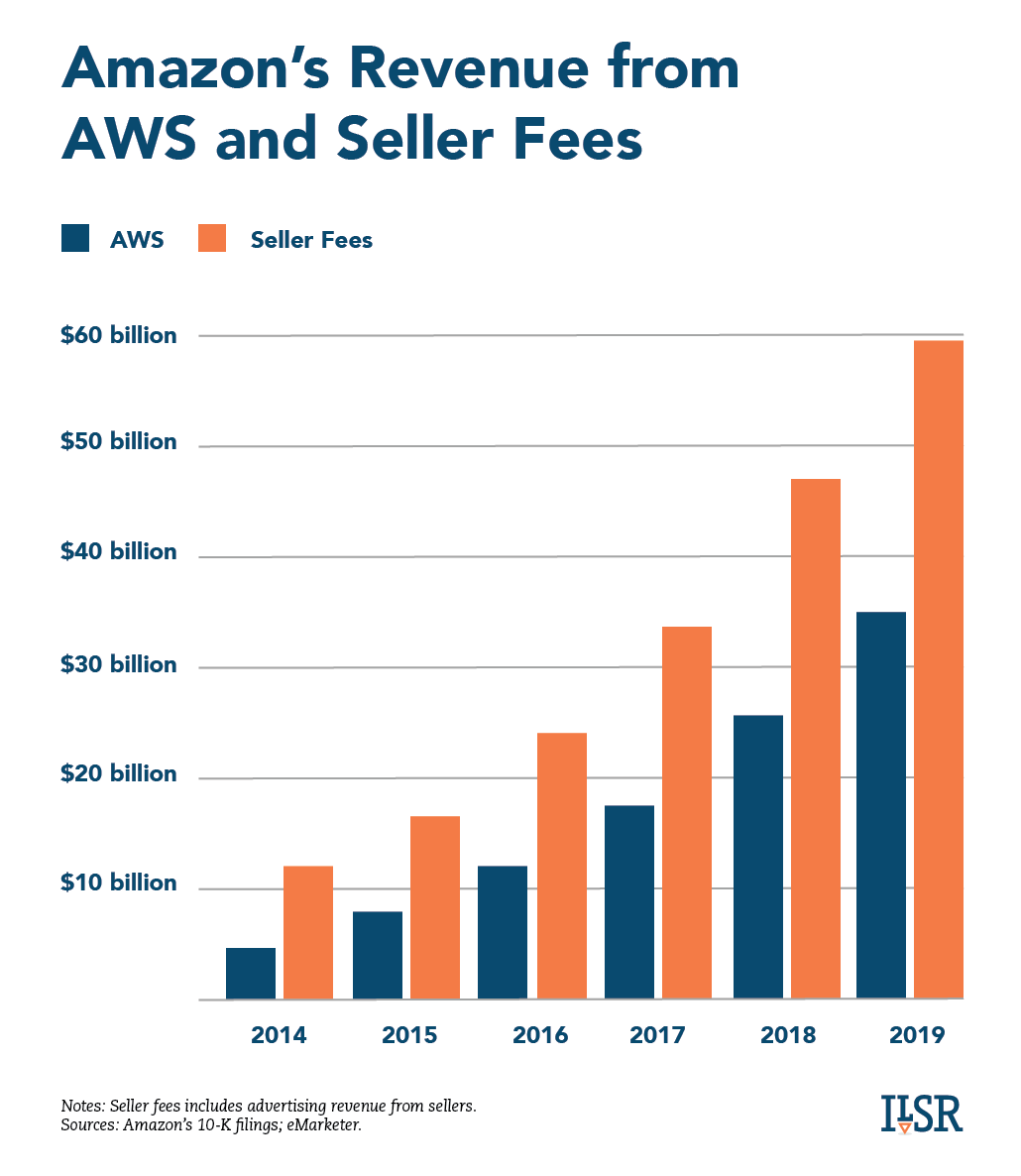

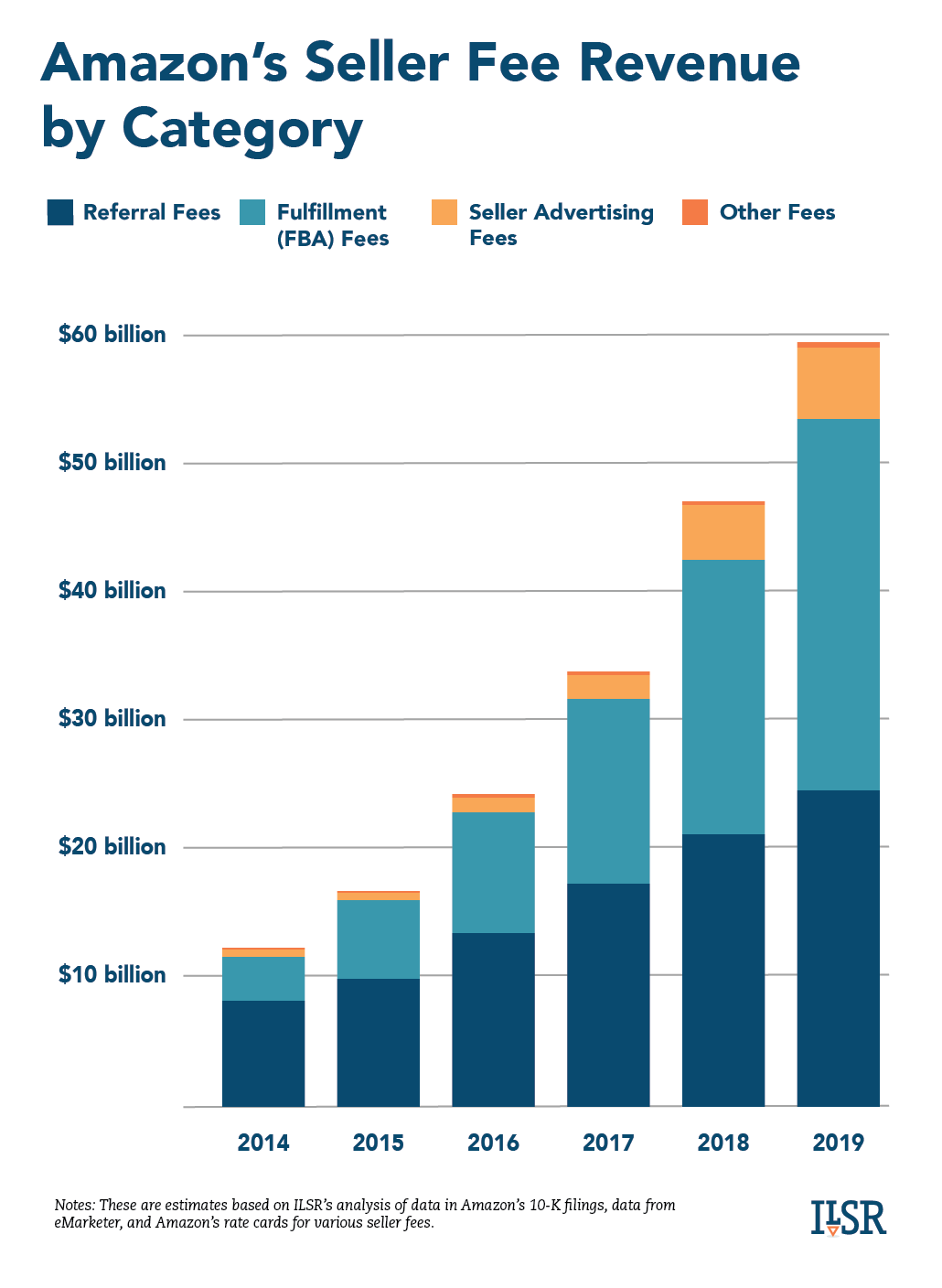

- Seller fees netted Amazon almost $60 billion in 2019, nearly double the $35 billion in revenue from AWS, Amazon’s massive cloud computing division.

- Since 2014, Amazon’s revenue from seller fees has grown almost twice as fast as its overall sales. Seller fees now account for 21 percent of Amazon’s total revenue.

- Amazon is extracting more from sellers by tying their ability to generate sales on its site to their willingness to buy additional Amazon services, including its fulfillment and advertising services.

- Amazon’s high fees make it nearly impossible for sellers to sustain a profitable business. Most fail. Yet Amazon has no risk of running out of sellers; its monopoly ensures there’s an endless stream of people, both here and abroad, willing to try.

- Amazon has leveraged its captive base of sellers to build a dominant logistics business. It’s now delivering half of the items ordered on its site and a growing share of those purchased on other sites. Amazon has already overtaken the U.S. Postal Service in the large e-commerce parcel market, and it’s expected to surpass UPS and FedEx by 2022.

- Amazon’s revenue from seller fees has grown so large that sellers are effectively cross-subsidizing Amazon’s retail division. Last year, seller fees covered more than three-quarters of Amazon’s total shipping and fulfillment expenses, including the costs of operating its warehouses, providing customer service, and processing payments.

- The policy solution to Amazon’s exploitation of its gatekeeper power must be twofold. First, its marketplace platform should be subject to public utility-like standards of non-discrimination and fair pricing. Second, its various divisions must be spun off into separate companies to eliminate conflicts of interest and monopoly leveraging.

If you like our research, sign up for our biweekly Hometown Advantage newsletter.

Doug Mrdeza remembers what life was like the year his company appeared on Inc. magazine’s list of America’s fastest growing private companies.

“It was like living the dream,” he says. “I loved doing what I did.” That was 2018. The tiny business Mrdeza had launched five years earlier out of his house in Lansing, Mich., had swelled to nearly 50 employees. Called Top Shelf Brands, the company was a modern, tech-infused iteration of a Main Street retailer. It sold hair care products online, mainly as a third-party seller on Amazon, and relied on algorithms to continually adjust prices and manage inventory. Top Shelf did more than $23 million in sales in 2018.

Today that seems like a distant dream. Mrdeza has had to lay off all but five employees and is working to avoid bankruptcy. What doomed Mrdeza’s business was Amazon’s market power. Like most e-commerce businesses, Top Shelf Brands has to go through Amazon to reach the vast majority of its customers. That’s because more than 60 percent of Americans who want to buy something online start their product search on Amazon, rather than a search engine.[1] In 15 of 23 major product categories, Amazon is capturing more than 70 percent of online transactions.[2] Although Top Shelf also sells on Walmart and eBay, these platforms are a very distant second and third in traffic to Amazon, and they generate only a small sliver of Top Shelf’s sales. In other words, Amazon so dominates online shopping traffic that it has become a gatekeeper.

As this report shows, Amazon is exploiting its gatekeeper power to siphon off a bigger and bigger cut of the revenue earned by independent sellers on its site. It’s doing this through the fees that it charges them. In effect, Amazon is levying a hefty tax on their trade — enabling it to profit from their businesses at the same time that it saddles them with more costs and thus weakens them as rivals. Over the last five years, Amazon’s revenue from seller fees grew roughly twice as fast as its overall sales. Seller fees netted Amazon almost $60 billion in 2019 — nearly double the $35 billion in revenue from its massive cloud computing division, Amazon Web Services (AWS).

These fees take three main forms. Referral fees are the cut that Amazon takes off the top of each sale by a third-party merchant. Then there are fees for two kinds of services that Amazon presents as optional, but sellers who buy them are given much more favorable positioning on the site and thus are significantly more likely to make sales. One is Fulfillment By Amazon (FBA), Amazon’s service for warehousing and shipping sellers’ products. The other is Amazon’s product advertising, which takes up a growing share of the space on its search results pages.

Through the combination of these fees, Amazon is keeping an average of 30 percent of each sale made by a third-party seller on its site. That’s up from 19 percent just five years ago. This increase in fees crippled Mrdeza’s business. As Amazon pocketed more of its revenue, Top Shelf slipped from being modestly profitable to losing money. Even as sales were soaring in 2018, Top Shelf was deep in the red. Mrdeza found that raising the prices of his products on Amazon’s site to account for these added costs wasn’t an option. That’s because if a seller offers a product at a higher price on Amazon than it charges on other platforms, Amazon penalizes the business by suppressing the visibility of its products and dramatically reducing their sales.[3]

(To read more of Mrdeza’s story, jump to the Sidebar at the end of this page.)

Mrdeza’s story is a familiar one to the tens of thousands of small businesses that have tried to succeed in an e-commerce market dominated by Amazon. The vast majority of those who start selling on Amazon’s site fail within a few years. Nearly two-thirds of third-party revenue on Amazon goes to sellers who began selling on the site within the last three years. Sellers who’ve been operating for five or more years account for only 10 percent of sales.[4] The way to understand this data is through the lens of Mrdeza’s experience: Sellers may appear to succeed at first, generating sales on the site, but soon find that Amazon’s fees and policies make it nearly impossible to sustain a profitable business. Selling on Amazon is like going to a casino: you might win a hand or two, but, in the end, only the house actually makes money.

Mrdeza’s story is a familiar one to the tens of thousands of small businesses that have tried to succeed in an e-commerce market dominated by Amazon. The vast majority of those who start selling on Amazon’s site fail within a few years. Nearly two-thirds of third-party revenue on Amazon goes to sellers who began selling on the site within the last three years. Sellers who’ve been operating for five or more years account for only 10 percent of sales.[4] The way to understand this data is through the lens of Mrdeza’s experience: Sellers may appear to succeed at first, generating sales on the site, but soon find that Amazon’s fees and policies make it nearly impossible to sustain a profitable business. Selling on Amazon is like going to a casino: you might win a hand or two, but, in the end, only the house actually makes money.

Amazon has argued that “if sellers weren’t succeeding, they wouldn’t be here,” in the words of Jeff Wilke, the chief executive of Amazon’s consumer business.[5] But in fact, between the large share of jobs that pay low wages and the many struggling brick-and-mortar retailers, there’s an endless stream of people in the U.S. hoping to build businesses selling online. And if that pipeline falters, Amazon already has another one in place. In 2013, the company began cultivating sellers in China and has set up an ocean shipping operation that allows sellers there to feed their goods directly into Amazon’s U.S. distribution system.[6] By January 2020, China-based sellers accounted for 49 percent of the top 10,000 sellers in Amazon’s U.S. marketplace.[7]

How Amazon Taxes Sellers to Fuel Its Monopoly Strategy

Last year, in his annual letter to shareholders, Amazon CEO Jeff Bezos reported that third-party sellers accounted for 58 percent of sales on Amazon, up from 46 percent five years before. Then, in reference to the growth of these sales relative to sales by Amazon’s own retail division (“first-party” sales), he said: “Third-party sellers are kicking our first-party butt.”

It was a smugly condescending remark, made from the vantage point of having firm control over the fates of third-party sellers. Through its algorithms, which control search and product pages, and its fee structures and other dictates, Amazon can steer consumers to third-party sellers, or to the products it’s selling itself, depending on which best serves its own interests. It has allowed third-party sales to grow because they’re extremely lucrative, and because Amazon can leverage its power over these smaller businesses to expand its market dominance.

With third-party sales, Amazon takes its cut right off the top, regardless of the seller’s costs and margins. It incurs none of the expenses of researching and sourcing products and investing in inventory, and carries none of the risk that the goods won’t sell. Just as Amazon uses temporary and “gig” workers to dodge costs and responsibility in its logistics operations, it uses third-party sellers to offload the expense of inventory, while profiting from their product knowledge, market insights, and entrepreneurial drive.

Our analysis finds that, last year, Amazon netted nearly $60 billion from the tolls it levied on third-party sellers, including referral fees, storage and shipping fees, advertising, and other charges.[8] That’s significantly more than the $35 billion in revenue the tech giant earned from Amazon Web Services (AWS), its massive cloud computing operation, which controls nearly half of the world’s public cloud capacity and provides the computing infrastructure for a huge number of corporations.[9] Seller fees accounted for more than one-fifth of Amazon’s total revenue in 2019, up from 14 percent in 2014.

Over the last five years, Amazon’s revenue from seller fees has grown two-and-a-half times as fast as total consumer spending on its site. In other words, Amazon’s fee revenue is increasing in large part because it is taking a larger cut of every dollar sellers make on the site. Five years ago, third-party sellers handed Amazon about $19 of every $100 in sales they made on the site. Today, it’s over $30.

Amazon’s profit margins on seller fees are about 20 percent, or four times higher than its margins on its own retail sales, according to analysts at Morgan Stanley.[10] Because of its market dominance, Amazon faces little risk of losing sellers to a competing platform if it overcharges. Its policy of penalizing sellers who charge less on other sites also means that Amazon’s fees are almost certainly being absorbed by consumers in the form of higher prices, not just on Amazon, but on other platforms as well.

Amazon’s revenue from seller fees has grown so large that sellers are now effectively cross-subsidizing Amazon’s retail division. The $59.5 billion that Amazon took in seller fees last year covered more than three-quarters of its total fulfillment and shipping expenses.[11] These expenses include most of Amazon’s e-commerce costs, including the costs of operating its distribution facilities, shipping and delivering products, providing customer service, and processing payments. This suggests that sellers cover the distribution expenses for their own sales and cover a substantial portion of Amazon’s first-party expenses. Amazon not only competes with sellers, it subsidizes that competition through the fees they pay.

As this report shows, Amazon’s exploitation of sellers is about more than extracting revenue from them. Amazon is also leveraging its dominance over sellers to gain market power in other sectors, furthering its monopoly strategy. Amazon has, for example, compelled sellers to buy its warehousing and fulfillment services in order to get the kind positioning on its site that leads to sales. Almost overnight this move has catapulted Amazon to being a top logistics provider without having to compete for it. Amazon has built a large digital advertising business in much the same way: by flexing its muscle over sellers and brands.

Amazon has faced growing scrutiny in recent months for spying on sellers and using the insights it gleans from them to develop its own competing versions of their products.[12] But Amazon’s monopoly strategy is far more complex and multidimensional than this single tactic suggests. By integrating its various divisions — marketplace, retail, private label, logistics, advertising, and more — Amazon gains multiple points of leverage, which it exploits with finesse. It leverages its private label products to pressure vendors to agree to its terms. It leverages its retail division to manipulate sellers in its marketplace. It leverages its marketplace to build a logistics empire. And, increasingly, it’s leveraging its logistics operation to fortify its monopoly in online retail.

Amazon has faced growing scrutiny in recent months for spying on sellers and using the insights it gleans from them to develop its own competing versions of their products.[12] But Amazon’s monopoly strategy is far more complex and multidimensional than this single tactic suggests. By integrating its various divisions — marketplace, retail, private label, logistics, advertising, and more — Amazon gains multiple points of leverage, which it exploits with finesse. It leverages its private label products to pressure vendors to agree to its terms. It leverages its retail division to manipulate sellers in its marketplace. It leverages its marketplace to build a logistics empire. And, increasingly, it’s leveraging its logistics operation to fortify its monopoly in online retail.

All of this suggests that policy solution to Amazon’s exploitation of the retailers and brands subject to its gatekeeper power must be twofold. First, its marketplace platform should be subject to public utility-like standards of non-discrimination, fair dealing, and reasonable pricing. And second, its various divisions must be spun off into separate companies to eliminate the conflicts of interest and monopoly leveraging that their integration invites and entails.

Amazon’s Baseline Tax: Referral Fees

Amazon’s baseline tax, called its “referral fee,” takes a cut from every sale made on its marketplace. It’s a tax no seller can avoid. For most products, Amazon’s cut is 15 percent. A few categories, such as clothing, have higher fees (17 percent), and a few, such as cameras, have lower fees (8 percent).

What’s remarkable about Amazon’s referral fees is that they’ve remained at the same level, more or less, for 20 years. When Amazon launched its Marketplace for sellers in 2000, its standard fee was 15 percent. [13] Since then, the corporation has grown a hundredfold. Given its low marginal costs — processing additional sales on the site creates very little additional expense – and ability to spread its fixed costs across far more transactions, Amazon’s growth should have yielded a decline in fees. And yet, Amazon’s 15 percent cut has held firm, suggesting that there is no competitive pressure for it to lower prices.

Molson Hart, chief executive of Viahart, a toy company, says Amazon’s high referral fees lead to higher consumer prices. He gives the example of a three-foot-long plush tiger toy, which retails on Amazon for $150. Between the $22.50 referral fee and another $17.58 Viahart pays in advertising costs so the tiger appears on Amazon’s search results page (more on this below), Amazon is keeping about $40 of each sale. “We designed, manufactured, imported, stored, shipped the item, and then we did customer service. Amazon hosted some images, swiped a credit card, and got $40,” Hart notes.[14]

In theory, Viahart could sell the tiger for just $113 on its own website and still make the same profit. But Amazon effectively blocks it from doing so. Under Amazon’s “fair pricing” policy, if Amazon detects a lower price for a product elsewhere, it will suppress the visibility and sales of the item on its site by demoting it in search results, deleting its Prime badge, or removing the “buy now/add to cart” buttons from the product page.[15] Viahart cannot afford to risk any of these actions: Amazon accounts for more than 90 percent of its sales.

The Tax that Built Amazon’s Logistics Empire: Fulfillment Fees

In 2006, Amazon launched Fulfillment By Amazon, or FBA.[16] Sellers who sign up for the service can send their items to Amazon’s warehouses and pay it to store, pack, and ship their orders.

During the early years of the program, relatively few sellers signed up for it. Many could obtain better rates or service from other warehouse operators and parcel carriers. Or they simply preferred to maintain control over their own inventory, shipping, and customer service, rather than turning over these functions to Amazon.

But beginning in 2011, factors other than price, service, and preference began to drive sellers to use FBA. That’s the year that Amazon began a serious push to grow Prime, its membership program, by adding a host of new perks. By 2013, the number of Prime members in the U.S. had grown to 25 million. Over the next three years, membership more than doubled, to 65 million in 2016, and then almost doubled again, to 112 million in 2019.[17]

But beginning in 2011, factors other than price, service, and preference began to drive sellers to use FBA. That’s the year that Amazon began a serious push to grow Prime, its membership program, by adding a host of new perks. By 2013, the number of Prime members in the U.S. had grown to 25 million. Over the next three years, membership more than doubled, to 65 million in 2016, and then almost doubled again, to 112 million in 2019.[17]

As more shoppers subscribed to Prime, they looked for products with the Prime badge, which Amazon would deliver in two days at no extra cost. This gave sellers a powerful reason to sign up for FBA: their items would qualify for the Prime badge and attract Amazon’s audience of Prime subscribers. To further prod sellers to use FBA, Amazon embedded a preference for those who use the service into its “buy box” algorithm. Its site uses this algorithm to control which seller is chosen as the default option for a particular product. This is known as securing the “buy box” and, with it, comes one-click ordering. It makes all the difference for a seller’s bottom line: more than 80 percent of the time, shoppers choose the default seller. Signing up for FBA makes it far more likely that a seller will “win” the buy box.[18]

In effect, Amazon made a seller’s ability to generate sales on its marketplace, which dominates e-commerce traffic, contingent on buying Amazon’s warehousing and shipping services. Not surprisingly, the number of sellers using FBA has risen rapidly. More than 85 percent of the top 10,000 sellers on Amazon rely on Prime shipping, up from 56 percent in 2016.[19] This kind of leveraging is known as “tying” in antitrust law. Amazon CEO Jeff Bezos has openly described the strategy. “FBA is so important because it is glue that inextricably links Marketplace and Prime. Thanks to FBA, Marketplace and Prime are no longer two things,” he wrote in his annual letter to shareholders in 2015. “Their economics…are now happily and deeply intertwined.”

Flexing its muscle as a gatekeeper to compel sellers to buy its FBA services has created a lucrative new revenue stream for Amazon. In its financials, Amazon does not break out seller fee revenue by category, but we estimate that FBA fees account for about half of Amazon’s fee revenue from sellers, and that its revenue from FBA fees has risen sharply over the last five years, growing from roughly $3 billion in 2014 to roughly $29 billion in 2019.

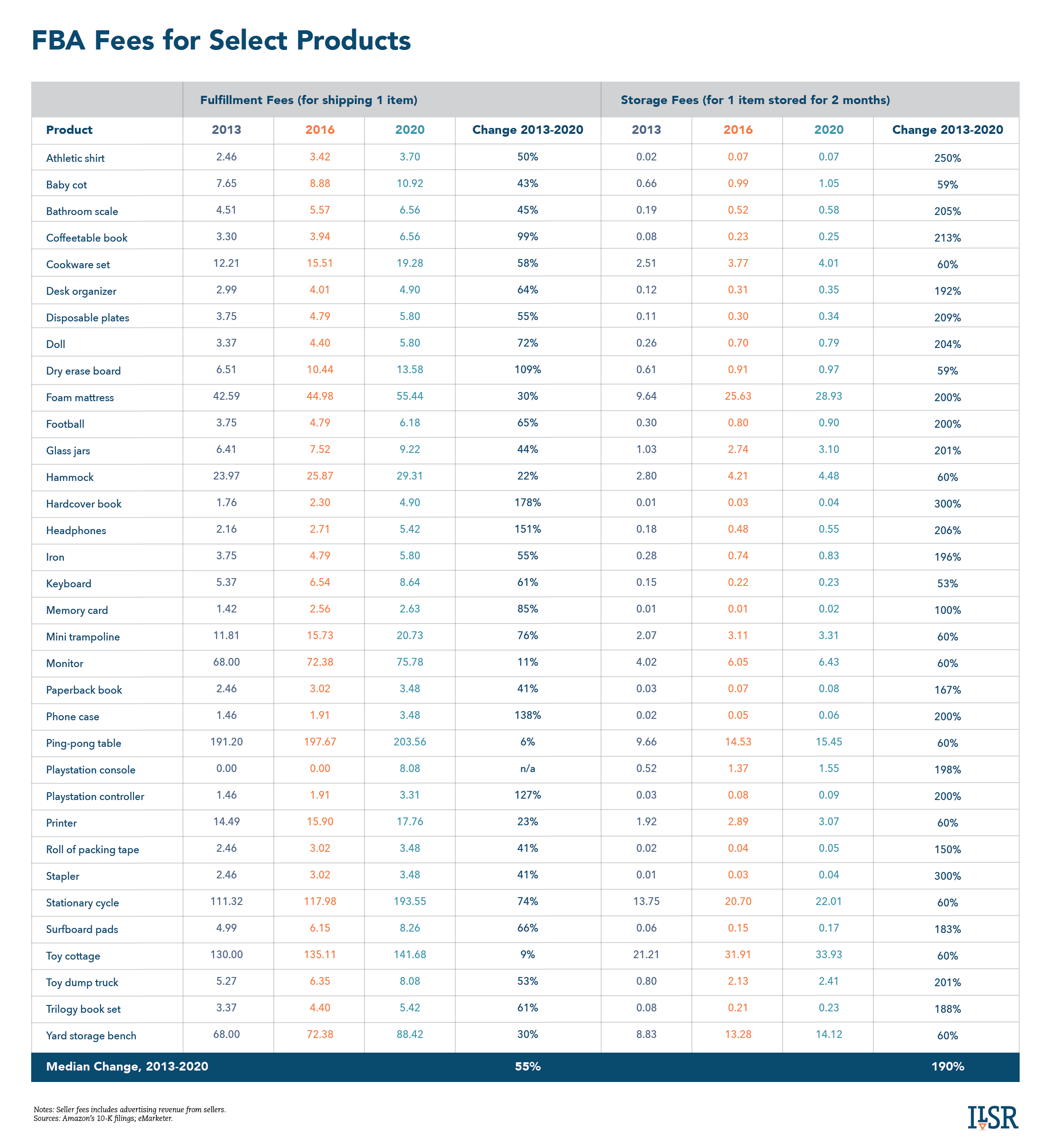

This growth has been driven in part by the increase in the number of sellers buying Amazon’s fulfillment services. It’s also been driven by a steep rise in the prices that Amazon charges for these services. Between 2013 and 2019, the standard rate for storing inventory in Amazon’s warehouses during off-peak months rose 67 percent. For the peak months of October through December, the rate soared by 300 percent. Storage rates for standard-sized items (those under 20 pounds and within certain dimensions) are now 75 cents per cubic foot per month during the first part of the year and $2.40 during the peak season. Amazon’s storage fees are much higher than those of its competitors, according to several sources.[20] A 2019 survey of 600 warehouses across the U.S. and Canada, for example, found an average rate of 50 cents per cubic foot.[21]

The prices Amazon charges to pack and ship an item have likewise risen. We took a diverse mix of 34 products — ranging from small items, such as a memory card, to larger items, such as a cookware set, to oversized goods, like a mini-trampoline — and calculated Amazon’s fees for shipping them in 2013, 2016, and 2020. Prices across the board went up. The size of the increase varied widely, but the median increase for an item was 55 percent. (See the table at the end of this report for the list of items and their FBA fees.)

“On a dollars and cents side, it’s not that competitive,” says Matthew White, a strategist with iDrive, a consulting firm that provides guidance to companies on their shipping options and helps them negotiate contracts with carriers. “I’d recommend Amazon if they were really good on price, but they’re not. If it weren’t for the algorithm, if it weren’t for the fifty-plus pressure points that Amazon is placing on the business, FBA wouldn’t be attractive.”

This tactic has enabled Amazon to rapidly gain market share in the logistics sector without having to compete for it. When Amazon first launched FBA, it stored products and packed orders in its warehouses, but relied on other carriers, including the U.S. Postal Service, UPS, and FedEx, to handle shipping and delivery. That’s changed. Today, a growing share of the products sold on Amazon are shipped by the company itself. Last year, Amazon delivered about half of its own packages, up from 15 percent just two years before.[22] To do this, Amazon has built hundreds of package sortation and delivery centers across the country, and it’s established its own network of contracted delivery providers who deliver packages solely for Amazon.

Thanks to its market power over sellers, Amazon’s logistics operation now rivals the top carriers in scale. In 2019, Amazon delivered 2.5 billion parcels, or about one-fifth of all e-commerce deliveries, according to an analysis by Morgan Stanley, which expects Amazon to overtake UPS and FedEx in market share by 2022.[23] It’s already overtaken the U.S. Postal Service, which, last year, saw its parcel volume fall for the first time in nearly a decade, adding to its financial woes.[24]

Amazon has thus leveraged its dominance over online shopping and its captive audience of sellers to rapidly become a huge player in package delivery – and it’s financed the necessary infrastructure on the backs of sellers. “It is a very effective way of driving their logistics business,” says White.

To further fortify its position in logistics, Amazon has curtailed Seller Fulfilled Prime (SFP), a program that allows elite sellers to earn the Prime badge if they can consistently meet the 2-day shipping time using other carriers. Amazon launched the program in 2015, before it had built out its own package delivery capacity. In February 2019, it stopped allowing new sellers to sign up.[25] Then, last fall, Amazon began threatening to revoke the Prime status of some SFP sellers, citing minor infractions, unless they switched from buying postage from the U.S. Postal Service to buying it from Amazon, often at higher rates.[26] Then in December, at the height of the holiday season, Amazon told SFP sellers that they could not ship Prime orders via FedEx’s ground service and could only use its more expensive express service.[27]

White says Amazon is pressuring his SFP clients by holding them to an on-time delivery rate of 98.5 percent, which is substantially higher than Amazon itself achieves. According to data from market-research firm Rakuten Intelligence, the share of Amazon packages arriving late tripled between 2017 and 2019, rising to 16.6 percent of orders.[28] But SFP sellers who have a few delays can suddenly find themselves losing their Prime badge or even having their selling accounts suspended altogether.

“It’s hell,” White says. “Your sales can fall by 50 to 60 percent overnight.” Often the only clear solution is to sign up for FBA. “That is the easiest way by far to make the nightmare be over.”

As Amazon becomes more dominant in logistics, it’s increasingly leveraging that dominance to further its monopoly power in online shopping. In other words, these two parts of Amazon are functioning as a monopoly feedback loop. Here’s one example of how this works. For many sellers, Amazon fulfills all of their orders, including those generated on other sites, such as EBay. This is because it’s not affordable or feasible for these small businesses to maintain sufficient inventory across warehouses in more than one system. Amazon compels them to use FBA and then charges much higher prices to pack and ship their “multi-channel” orders. It charges 66 percent more, for example, to ship a modestly sized item, such as a shirt or a book, purchased on EBay than one ordered on Amazon. Through its logistics division, Amazon bolsters its e-commerce dominance by raising the cost of selling on other platforms, while also reaping valuable insights about sales made through these other channels.

These two divisions — FBA and Marketplace — work in tandem to entrench Amazon’s power in e-commerce and build its power as a warehousing and shipping service. “It’s not just about money. It’s about control,” White says. “Amazon knows it can always be getting maximum value if it controls that entire chain from payment through delivery.”

Tightening the Screws: Sponsored Product Advertising

Amazon’s advertising business is its latest tool for squeezing more revenue from the small businesses that depend on its site to reach customers. Just as Amazon has done with its fulfillment business, it is increasingly tying a seller’s ability to generate sales, and thus its survival, to the purchase of advertising on its site.

Amazon launched its digital advertising business in 2012, but only began to focus on growing it in the last few years. Most of the company’s ad revenue comes from sponsored brand and product advertisements — the ads that typically appear on its search results pages, usually at the top of the page and also interspersed with the products featured by Amazon in its organic search results. These ads ensure that the first thing a customer sees are products from sellers and brands that bought the space.

Over the last few years, Amazon has converted a growing share of the real estate on its search results pages to sponsored products, while reducing the space devoted to organic results.[29] As a consequence, sellers that do not advertise are generating fewer clicks on their product pages. Between 2017 and 2019, the share of product page views that came from customers clicking on ads nearly tripled, rising from 4 percent to 11 percent.[30]

Amazon doesn’t break out its advertising revenue separately, but according to eMarketer, advertising accounts for more than 70 percent of the revenue in its “Other” category and most of its ad revenue comes from sponsored listings on its site.[31] Assuming that third-party sellers’ share of this revenue equals their share of retail sales on Amazon’s platform, we estimate that Amazon’s advertising revenue from sellers has grown from about $1 billion in 2016 to nearly $6 billion in 2019. (The remainder of Amazon’s sponsored advertising revenue comes from brands that are supplying Amazon’s retail division as vendors.)

As with every component of Amazon’s marketplace strategy, its advertising business is structured to reinforce its other mechanisms of dominance and extraction. Sellers cannot, for example, advertise a product unless they have secured the “buy box” for that item — that is, they’ve been chosen by Amazon’s algorithm to be the one-click shopping option for that product.[32] As we discussed above, sellers that buy Amazon’ fulfillment services stand a better chance of winning the buy box. To succeed, then, sellers not only need to buy the advertising, but in many cases they also need to buy Amazon’s fulfillment services; otherwise their ads won’t actually appear in the search results.

Sellers that decline to advertise risk losing their place in Amazon’s organic search results, no matter how many glowing customer reviews they have. That’s because the Amazon algorithm that delivers the search results favors products with more sales. As more orders are driven by ads, sellers than don’t advertise lose out on those sales and, as their share of sales declines, they also slip in the search rankings, further reducing their sales in a negative cycle.

As the pressure on sellers to buy advertising has grown, so too has the cost of the ads. Amazon sets its ad prices through a reverse auction, so small businesses have to bid on keywords that customers enter in search. Over the last year, the cost-per-click for sponsored ads increased by about 15 percent on average.[33] But the price of some keywords has skyrocketed. The cost of advertising on the results page for “laundry detergent liquid” rose 127 percent, for example.[34]

Amazon also advertises its own private-label products, which reduces the space available for sponsored listings, helping to drive up ad prices for independent sellers and brands. While the brands and sellers that compete with Amazon have to pay for sponsored listings, Amazon allocates this space to its private-label product division for free.[35] It’s one more way that Amazon uses its platform to cross-subsidize its Retail division.

Amazon’s Nickels and Dimes: More Fees

While these are the primary ways Amazon taxes third party sellers that rely on its marketplace, it’s far from the only way Amazon nickel-and-dimes the small businesses it claims to champion. If, for example, sellers want access to an account manager — that is, they want to be able to talk with an Amazon employee when they need an answer to a question or help navigating the byzantine rules of the Marketplace — Amazon charges as much as $5,000 per month.[36] The fee amounts to a protection racket; sellers feel compelled to pay, as any glitch or a suspended account can have ruinous consequences for sellers without an account manager to help. As one seller complained in Amazon’s forums, “It seems wrong that we should have to pay Amazon for this service, but there you go.”

If a seller wants Amazon to collect sales tax for it, Amazon will – and it will take another percentage cut of each sale for doing so. In other words, sellers are made to pay an Amazon tax on top of the actual tax. It’s a service that eBay, for example, provides for free, but Amazon’s dominance as a retail platform allows it to charge sellers whatever it likes.

Conclusion: Policy Solutions

Amazon controls the underlying infrastructure for a large and growing share of our economy. Its dominance of e-commerce makes it a gatekeeper to the market for countless online sellers. This extraordinary position allows Amazon to, in effect, tax the transactions of businesses that depend on this infrastructure. Through its fees, Amazon extracts a growing share of its sellers’ revenue, fortifying its own dominance at their expense. At the same time, it leverages its control over sellers to gain power in new, adjacent industries, such as fulfillment and advertising, without having to compete for it. By integrating across business lines, Amazon can perpetually expand its monopoly power and exploit it with finesse.

The policy solutions to Amazon’s exploitation of the retailers and brands trapped by its gatekeeper power must be twofold.

First, its marketplace platform should be subject to public utility-like standards of non-discrimination, fair dealing, and reasonable pricing. Congress should instruct an agency, such as the Federal Trade Commission, to establish rules for dominant digital platforms to ensure that Amazon provides fair and reasonable terms and pricing for sellers and cannot use its gatekeeper power to privilege favored firms or impose onerous costs on market participants.[38]

Second, Amazon’s various divisions must be spun off into separate companies to eliminate the conflicts of interest and monopoly leveraging that their integration invites and entails. Congress should adopt a policy mandating that dominant digital platforms spin off their other divisions as separate, stand-alone companies. This would separate Amazon’s various components — its online marketplace, retail division, logistics operation, and so on — into separate companies.

Structural separation was once “a standard regulatory tool and key antitrust remedy in network industries,” applied in industries including railroads, bank holding companies, television networks, and telecommunication carriers.[39] Today, the inherently anti-competitive dynamics of Amazon, including its ability to appropriate revenue and data from businesses that depend on its platform, and to manipulate platform outcomes to entrench its market power and advantage its other lines of business, call for picking up this tool once again.

SIDEBAR: The Short Lifecycle of a Third-Party Seller

Before starting Top Shelf Brands, Doug Mrdeza had been a barber. The hair care products he stocked in his shop didn’t always sell, and that’s how he found his way into online retail. One day he decided to try selling surplus jars of pomade on eBay. It worked. Soon Mrdeza was spending some of his evenings selling on eBay, boxing up and mailing goods as the orders came in. But selling on eBay was a small sideline; it didn’t generate enough income to leave his day job. Then, in 2014, he heard about Fulfillment By Amazon, or “FBA,” a program that allows companies like his to send their inventory to Amazon and let it handle the packing and shipping. “I sent in enough inventory for what would normally be a month of sales,” Mrdeza recalls. “It was gone in an hour.”

On Amazon, Mrdeza’s business took off. More than a dozen brands partnered with Top Shelf to represent their products on Amazon. The company outgrew one space in Lansing, and then another, eventually expanding to more than 45 employees. “I felt great being an employer and providing a living for people,” Mrdeza says. A job at Top Shelf came with health insurance and a 401k plan. “We’re not the kind of people who want to take this money and put it in our jeans,” Mrdeza says of his management team. “We want everyone to do well.”

Top Shelf Brands seemed to be the picture of what Amazon claims it does for small businesses. Amazon features small businesses heavily in both its marketing and its lobbying. Amazon says that it enables entrepreneurs to “follow their dreams” and that many are “thriving” by selling on Amazon.[37] Mrdeza himself was one of Amazon’s top boosters. “I used to tell everyone how great Amazon is,” he says.

But in 2018, even as his sales were soaring, Mrdeza’s business was failing — in large part because of Amazon itself. Amazon was pocketing a growing share of Top Shelf’s sales through the fees it charged the company. The fees for FBA, Amazon’s warehousing and shipping service, had shot up. And, as Amazon turned over more of the real estate on its site to sponsored product ads, Top Shelf found it had to buy ads from Amazon to reach customers, which meant more fees.

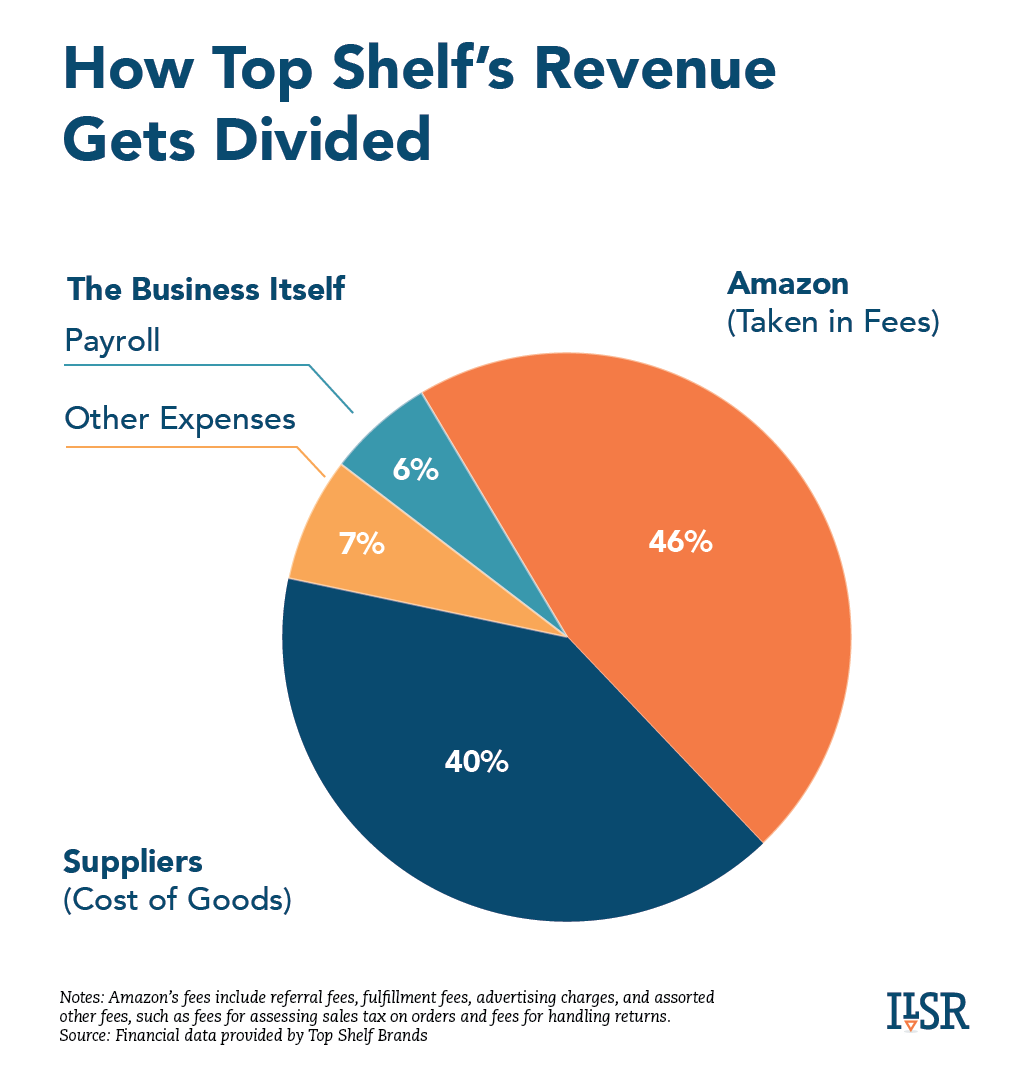

When Mrdeza was just starting out, in 2014, Amazon fees ate up 35 percent of Top Shelf’s revenue. By 2018, Amazon’s cut had swelled to more than 46 percent. After Top Shelf paid its suppliers, that left just 13 percent of its revenue to cover payroll and the rest of its expenses. In other words, Amazon was netting significantly more revenue from Top Shelf’s business than the company and its employees were. Top Shelf eked out a modest profit in 2016 and 2017, but by 2018, it was losing money. Although Mrdeza tried to expand sales on other platforms, such as EBay, and its own site, more than 90 percent of its revenue was coming from Amazon.

On top of paying Amazon’s rising tolls, Mrdeza and his staff were spending a lot of time correcting errors in Amazon’s system — errors that always seemed to fall in Amazon’s favor. Top Shelf would ship 220 units of a hair gel to an Amazon warehouse, but only 200 would show up as inventory in Seller Central, Amazon’s portal for sellers. Getting the other 20 accounted for would require filing a case through Amazon’s opaque in-house adjudication system. Or sometimes Amazon would suddenly start charging $3.03 to pack and ship an item that it had been shipping for $2.50. Top Shelf would log a case in Seller Central asking Amazon to measure the item again, and the price would come back down. But then Top Shelf would have to file another case requesting a refund for the overcharges.

At some point, Mrdeza realized that he could hire an engineer to write code to analyze the data and automatically file cases when there was a discrepancy. But then he learned that Amazon, famous for running its far-flung empire with complex algorithms that govern everything from product pricing to employee terminations, doesn’t allow sellers to use automated programs to create cases within Seller Central.

If you “actually add up all the ways Amazon nickels and dimes you… you can’t make money,” Mrdeza says. With the business deep in the red, Mrdeza spent 2019 trying to right the ship — but, he says, Amazon’s heads-we-win, tails-you-lose policies have made it impossible.

TABLE: FBA Fees for Select Products

[1] “Three-fourths of consumers go to Amazon when they are ready to make a purchase,” Feedvisor, Mar. 19, 2019; ”More Than 50% of Shoppers Turn First to Amazon in Product Search,” Spencer Soper, Bloomberg, Sep. 27, 2016.

[2] “An eCommerce Year in Review: Jumpshot Reveals Retail Winners, Losers and Amazon Data Report,” Jumpshot Press Release, Jan. 31, 2019.

[3] “Amazon Squeezes Sellers That Offer Better Prices on Walmart,” Spencer Soper, Bloomberg, Aug. 5, 2019.

[4] “Longtime Amazon Sellers Drive Most Sales,” Marketplace Pulse, June 30, 2020.

[5] “Prime Power: How Amazon Squeezes the Businesses Behind Its Store,” Karen Weise, New York Times, Dec. 19, 2019.

[6] “Amazon helps Chinese merchants double their sales on Amazon sites in 2015,” Frank Tong, Internet Retailer, Dec. 9, 2015; “Will Amazon Kill FedEx? For UPS and FedEx, Amazon’s been great for business. Now it’s taking business away from them,” Devin Leonard, Bloomberg, Aug. 31, 2016.

[7] “Chinese Sellers Outnumber US Sellers on Amazon.com,” Marketplace Pulse, Jan. 23, 2020.

[8] Amazon’s financials break out revenue from third-party seller fees, but do not include seller payments for product advertising. ILSR has estimated those fees and included them here. Our estimates are based on data from eMarketer and information from Amazon’s financials.

[9] “Amazon owns nearly half the public-cloud market,” MarketWatch, July 30, 2019.

[10] “Amazon’s Third Party Needs to Keep Raging,” Dan Gallagher, Wall Street Journal, Oct. 7, 2018.

[11] Amazon’s 10-K reports its fulfillment expense at $40.2 billion and its shipping costs at $37.9 billion.

[12] “Amazon Scooped Up Data From Its Own Sellers to Launch Competing Products,” Dana Mattioli, Wall Street Journal, April 23, 2020.

[13] “Amazon Courts the Small Vendor In Hopes of Being the Other eBay,” Nick Wingfield, The Wall Street Journal, July 22, 2002.

[14] “How Amazon’s Business Practices Harm American Consumers: Why Amazon Needs a Competitor and Why Walmart Ain’t It,” Molson Hart, Medium, Jul 18, 2019

[15] “Amazon Marketplace Fair Pricing Policy,” available at https://sellercentral.amazon.com/gp/help/external/G5TUVJKZHUVMN77V, viewed July 23, 2020. Also see: “Amazon Squeezes Sellers That Offer Better Prices on Walmart,” Spencer Soper, Bloomberg, Aug. 5, 2019.

[16] “Amazon Launches New Services to Help Small and Medium-Sized Businesses Enhance Their Customer Offerings by Accessing Amazon’s Order Fulfillment, Customer Service, and Website Functionality,” Amazon Press Release,

Sept. 19, 2006.

[17] Data on Prime membership in the U.S. is from Consumer Intelligence Research Partners.

[18] “How Amazon Rigs Its Shopping Algorithm,” Stacy Mitchell and Shaoul Sussman, Promarket, University of Chicago’s Stigler Center, Nov. 6, 2019.

[19] “Number of Amazon Sellers Offering Prime Up 50% in Three Years,” Marketplace Pulse, Nov. 7, 2019.

[20] See for example: “Prime Power: How Amazon Squeezes the Businesses Behind Its Store,” Karen Weise, New York Times, Dec. 19, 2019.

[21] “Warehousing and Fulfillment Fees Rise According to Latest insightQuote Survey,” WarehousingAndFulfillment.com, Feb. 26, 2019.

[22] “Amazon, the new king of shipping,” Erica Pandey, Axios, Jun 27, 2019.

[23] “Amazon Logistics parcel volume will surpass UPS and FedEx by 2022, Morgan Stanley says,” Emma Cosgrorve, Supply Chain Dive, Dec. 13, 2019

[24] “Postal Service Reports First Drop in Packages in Nearly a Decade,” Paul Ziobro, Wall Street Journal, Aug. 9, 2019; “Amazon, the new king of shipping,” Erica Pandey, Axios, Jun 27, 2019.

[25] “Responses to Questions for the Record following the July 16, 2019, Hearing of the Subcommittee on Antitrust, Commercial, and Administrative Law, Committee on the Judiciary, Entitled “Online Platforms and Market Power, Part 2: Innovation and Entrepreneurship”,” United States House of Representatives Document Repository, October 11, 2019

[26] “Amazon Bars Use Of USPS Delivery Service For Some Seller-Fulfilled Goods,” FreightWaves, November 13, 2019

[27] “Amazon blocks sellers from using FedEx ground-delivery shipping,” Annie Palmer, CNBC, Dec. 16, 2019.

[28] “Amazon is moving away from USPS and UPS for its in-house delivery network — but the ‘sloppier’ system may be delaying your packages,” Rachel Premack, Business Insider, July 3, 2019

[29] “Amazon is stuffing its search results pages with ads,” Rani Molla, Vox, Sep 10, 2018.

[30] “More of the products you view on Amazon are coming from ads,” Rani Molla, Vox, Sept. 16, 2019.

[31] “Amazon’s Ad Business May Be Growing Faster Than Thought,” Alexandra Bruell, Wall Street Journal, Feb. 20, 2019.

[32] “Amazon Sponsored Products: Everything You Need To Know (2020),” AdBadger, June 3, 2020

[33] “Prices for Amazon Sponsored Product Ads Continue to Climb,” Nicole Perrin, eMarketer, February 20, 2020

[34] “Amazon puts a dent in Google’s ad dominance,” Suzanne Vranica, MarketWatch, April 4, 2019

[35] United States House of Representatives Document Repository, “Responses to Questions”

[36] “Strategic Account Services – Core,” Amazon, accessed July 28, 2020

[37] “Small business means big opportunity: Amazon’s 2019 small business impact report,” Amazon, May 2019.

[38] See: “Comments of Stacy Mitchell, Institute for Local Self-Reliance to the U.S. House of Representatives Committee on the Judiciary Subcommittee on Antitrust, Commercial and Administrative Law Investigation into Competition in Digital Markets,” May 4, 2020.

[39] “The Separation of Platforms and Commerce,” Lina M. Khan, Columbia Law Review, Vol. 119, No. 4.

If you like this post, be sure to sign up for the biweekly Hometown Advantage newsletter for our latest reporting and research.