How to Fix the Country’s Biggest Power Market — Episode 248 of Local Energy Rules

The high prices being paid to power plant owners by power market operator PJM in the competitive wholesale electricity market in the mid-Atlantic region have policymakers screaming about the need for solutions to keep electricity affordable. Could one option be letting utilities back into power plant ownership?

For this episode of the Local Energy Rules Podcast, host John Farrell is joined by Tyson Slocum, Energy Program Director at Public Citizen.

Listen to the full episode and explore more resources below — including a transcript and summary of the episode.

The Electricity Sticker Shocks Stalking the Mid-Atlantic

“We end up putting corporate interests in the driver’s seat, and I just don’t think that works.”

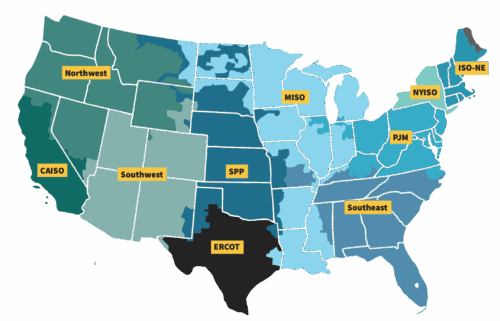

PJM is the country’s largest power market. It stretches from Illinois to the Mid-Atlantic, and right now, Tyson Slocum says, it’s in crisis.

The most pronounced place this crisis is playing out is through PJM’s wholesale capacity auction, where generation owners bid on producing capacity for a short window. Power plant owners developed capacity auctions because they complained the energy-only market did not provide enough revenue to incentivize new construction.

And now the region’s capacity auction prices are exploding, with a recent auction surpassing $16 billion. Essentially, Slocum explains, this sum represents a transfer of wealth to power generation owners, with electricity consumers picking up egregiously high price increases.

“We need a lot more transparency and accountability into who is making the money and whether or not those massive profits and windfalls are actually translating into more reliable service. And I think the answer is it’s not. I think we’ve got a broken market system.”

Why the PJM Capacity Market is Broken

“You still have too many regulators that are looking at the day when they are no longer a regulator and want to cash in and work for the utility.”

Behind the highly visible sticker shocks confronting customers is a history of corporate greed coupled with regulatory failure.

For one, corporate interests dominate PJM’s internal governance system. These interests constantly tweak complex power market rules to their own benefit, keeping electricity prices high.

Second, Slocum explains how the Federal Energy Regulatory Commission (FERC) has encouraged lighter handed regulation, which places corporate interests in the driver’s seat. The outcome is lousy transparency and minimal accountability.

“Because of our politics and the way that our democratic republic privately finances elections and allows significant roles for vested interest lobbyists among other things, we’ve got regulators that too often side with a utility shareholder interest and not the public interest.”

Getting In On Generation

“Utilities are seeking to get back into the generation game first and foremost because they think Wall Street will reward them.”

Lured by the astronomical capacity auction figures, regulated utilities in the PJM market are now looking to become power generation owners so they can get in on the lucrative action.

They know Wall Street will reward them with guaranteed, steady returns from rate-based assets, like power plants. These predictably steady returns drive utilities’ financial incentive to overestimate future demand as overbuilding capacity increases profits and dividends for shareholders.

Slocum also cautions that the new push toward new fossil gas power plants poses an enormous risk. Record exports of liquified natural gas have driven up demand, meaning the era of cheap natural gas has effectively ended, he says. Utilities advocating for new gas generation are essentially committing their ratepayers to massive future costs and extremely expensive stranded assets.

Putting All the Options on the Table

“I really question whether privately owned transmission assets are a viable solution right now.”

Slocum advocates for several fixes, emphasizing the need for principled regulators who prioritize the public interest. These authorities, he says, have to establish a clear mandate to deliver least-cost, reliable, zero-emission resources, and must conduct robust, independent demand assessments. They cannot take at face value the inflated projections that utilities and Big Tech push.

Instead of building new plants, the most effective solutions, he explains, involve better demand management, and deploying cost-effective measures like energy efficiency and demand response. Utilities need to focus on more effectively “managing demand and providing incentives to help make that happen.”

Slocum calls for expanding intervenor funding, where “qualified experts and qualified organizations are able to get financially reimbursed for their costs [of participating in rate cases] just as utilities get to do every single day.” He also supports publicly owned or not-for-profit utility models to eliminate the conflict between corporate profit and public duty.

“You have this constant tension between their corporate desire to return profits to their shareholders and their legal and regulatory responsibilities to rate payers and the public interest.”

How States Can Fight Federal Headwinds

Slocum suggests there may not be the political capital to do a wholesale overhaul of the complex utility system. Additionally, Slocum predicts that future federal intervention, especially under a Trump administration’s politicized FERC, will be destructive and counterproductive to affordability and renewables.

Given anticipated hostile federal interference, Slocum says states should explore strategies to insulate their utilities from federal intrusions. They should consider creating new regional market structures where governance aligns with local goals on affordability and emissions reduction, pointing to systems in California or Texas as examples.

Bringing it back to the PJM crisis, Slocum says he sees an opportunity for states to peel away from PJM to create new governance structures that prioritize state interests, particularly around affordability and greenhouse gas reductions.

“We need better regulators at FERC, we need better regulators at the state level, and we can figure out with those better regulators a path forward that holds vertically integrated utilities more accountable.”

Episode Notes

See these resources for more behind the story:

ReadILSR’s report, Upcharge, which provides an overview of the broader tension between utility profits and consumer interests.

Listen to Local Energy Rules episode 223 with Patrick Robbins, discussing New York’s approach to having public ownership of new power generation.

This is the 248th episode of Local Energy Rules, an ILSR podcast with Energy Democracy Director John Farrell, which shares stories of communities taking on concentrated power to transform the energy system.

Local Energy Rules is produced by ILSR’s John Farrell and Ingrid Behrsin. Audio engineering by Drew Birschbach. Featured Photo Credit: FERC.