Download the Report

Executive Summary

Energy efficiency and renewables represent the most promising pathway to lower energy costs for individual consumers and utilities. Programs that help utility customers pursue home improvements, like better insulation or rooftop solar panels, can slash monthly utility bills and eliminate the need for utilities to add costly — and outdated — power and gas infrastructure. The upside is undeniable, with energy efficiency measures alone predicted to save customers $2 trillion by 2030. But limited access hinders progress. The best energy efficiency programs serve less than 2% of customers each year, and few reach the majority of a utility’s customers, including renters, customers without strong credit, and low- and moderate-income households, who pay disproportionately high energy bills.

Utilities can knock down major barriers to energy efficiency and renewables by allowing customers to make site-specific investments and recovering utility costs through an opt-in tariff. Tariffed on-bill programs are often referred to as inclusive financing because they allow all utility customers the option to access cost effective upgrades. Inclusive financing solves many of the problems dogging the push for a more sustainable, affordable, and equitable energy economy because, unlike loan-based programs, tariffed on-bill programs are open to all customers regardless of their income, credit score, or renter status.

The Opportunity:

When a utility supports energy-savings efforts by offering to invest in upgrades rather than offering traditional debt financing, there are five major benefits:

- Immediate Savings – well designed on-bill programs result in energy savings that deliver bill savings each year from the beginning.

- Universal Access – unlike debt-based financing programs that don’t serve customers with lower credit scores, inclusive financing programs serve all customers regardless of income, credit score, or renter status.

- Simplicity – with no loans to customers, inclusive financing makes investments in energy efficiency and on-site renewable energy much easier to access through utilities that can recover costs on the monthly bill.

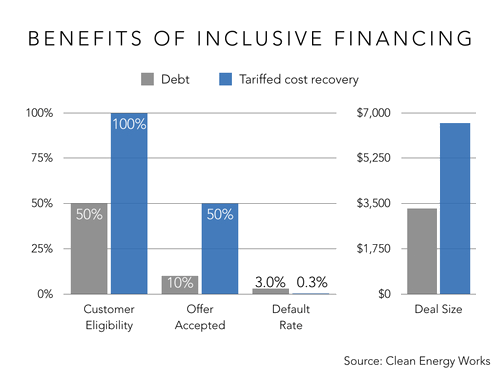

- Bigger Savings – customers tend to accept energy improvement projects that are twice as big when offered inclusive financing with a tariff agreement compared to a personal loan.

- Low Risk – utilities that offer inclusive financing report charge-offs that are less than one-tenth the national default rate for unsecured consumer loans.

A Huge Opportunity

The opportunity to reduce energy consumption and related costs by boosting energy efficiency and renewables is staggering.

By 2030, the U.S. Department of Energy estimates, a mounting push for efficiency will reduce energy use enough to slash electricity customers’ bills by $2 trillion. Residential customers alone may see as much as $15.4 billion in savings by 2030 in the northeastern U.S., with individuals owning energy-efficient homes cutting their bills by 25 to 35 percent over 15 years.

Rooftop solar can help reduce costs, too. If the maximum number of residential and commercial rooftops were covered with panels, it could cut residential electric bills by over $72 billion and commercial bills by $58 billion, based on average retail electricity prices. The individual savings are significant, too. In Minnesota, for example, a homeowner can generate between $13,000 and $28,000 over 20 years with rooftop solar.

The benefits multiply when the calculus factors in benefits to the energy system. Lower on-site use and higher local energy production reduce demand, translating to a longer life for existing distribution and generation infrastructure and reducing the need for new power plants.

In addition, a booming energy efficiency sector drives job growth, as does distributed solar.

The upside presented by energy efficiency and distributed renewable energy is stoking an appetite for communities to maximize these financial and wider economic benefits, and to distribute them widely. Boulder, CO, has sought to take over its electric utility and amplify local public benefit. Minneapolis, MN, forged a unique partnership with two utilities to advance its Climate Action Plan, tailored to promote a clean, local, equitable, and affordable energy future. It’s likely only the beginning.

Challenges to Reaching Most Customers

Many cities, like Minneapolis, have ambitious goals for reducing energy use. The Minneapolis Climate Action plan sets the goal of reaching 75% of single- and multi-family customers with home energy services by 2025. With about 10% already served by existing programs, approximately two-thirds of electric and gas customers must be reached in the next 10 years to meet the goal.

Overall, even in the best efficiency and renewable programs, only about 1-2% of customers take advantage of energy savings opportunities each year. Information on many programs is limited to bill inserts or marketing that may fail to reach many customers, especially low-income customers. One California study, for example, found utilities had trouble reaching customers “that were non-white, lower-and middle-income, non-college educated, or non-English-speaking.” Even when the message reaches customers, the complexity of identifying contractors, finding financing, or enduring work on their property becomes an insurmountable barrier.

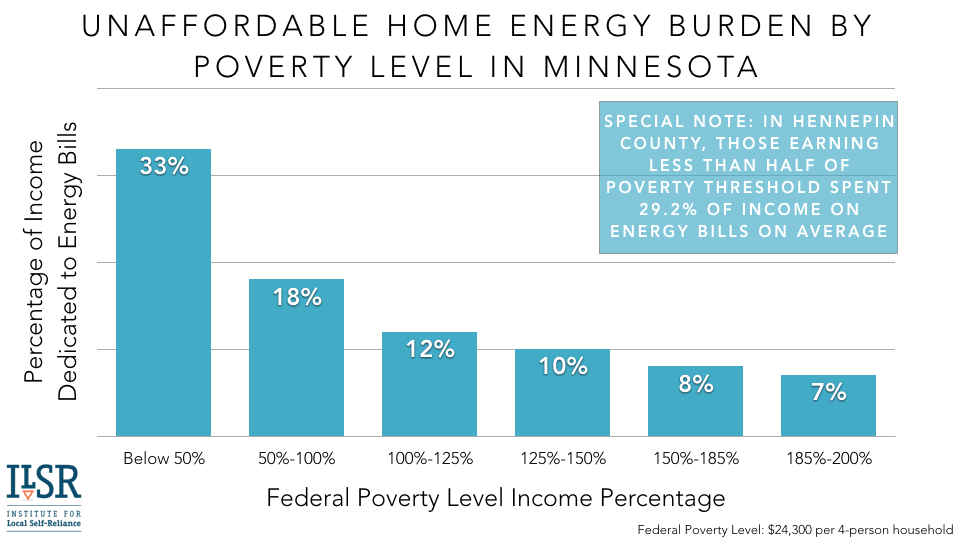

Low-income customers are often shut out of programs even though they shoulder the heftiest utility bill burden. In fact, those households spend up to three times as much of their income on energy charges as their higher-wage counterparts. The trend persists even when energy prices sink, because low-income customers tend to live in older, less-insulated homes. For example, households in Minnesota’s Hennepin County (which includes Minneapolis) whose income falls below 50 percent of the federal poverty level spend an average of 29.2 percent of their earnings on energy costs, well beyond the 6 percent threshold that is considered affordable. That’s nearly $2,050 per year.

Meanwhile, the gulf is widening between what is considered affordable and what Minnesotans (and residents of other states) actually pay for energy. The gap grew from $652 million in 2011 to $675 million in 2015, according to national research firm Fisher Sheehan & Colton, an energy affordability watchdog. Just bringing the homes of low-income residents up to the average level of home efficiency in the U.S. would help them enormously, reducing energy costs by one-third.

Due to the stratification of income in the U.S. by race, bringing the homes of low-income residents up to the average level of efficiency would particularly reduce energy burdens for people of color. “For African-American and Latino households, 42 percent and 68 percent of the excess energy burden, respectively, would be eliminated,” says one report.

The following graphic illustrates the swath of population typically unable to access loan-based efficiency or renewable energy programs — renters and those with subprime credit — but who can be served with tariff-based financing.

To get there, the status quo is not sufficient. Existing programs aren’t reaching a majority of the customers, and persistent barriers to participation – like cash requirements to access rebate programs or willingness to take on debt for loan programs – affect market segments that extend far beyond low-income households.

A Necessary Paradigm Shift

For decades, most U.S. electric and gas utilities have operated as monopolies, with revenue rooted in building new infrastructure and selling more energy. Regulators tend to defer to utility plans for the electric and gas grids — plans that have only modestly shifted from the historic priority to build more and sell more.

Last century’s business model no longer works in an economy where customers have more choice in the energy they use — by supplanting utility electricity with rooftop solar, for example. Energy efficiency standards have dramatically lowered the energy consumption of large appliances, and technology advances have reduced power consumption as well as the size of many electronic devices.

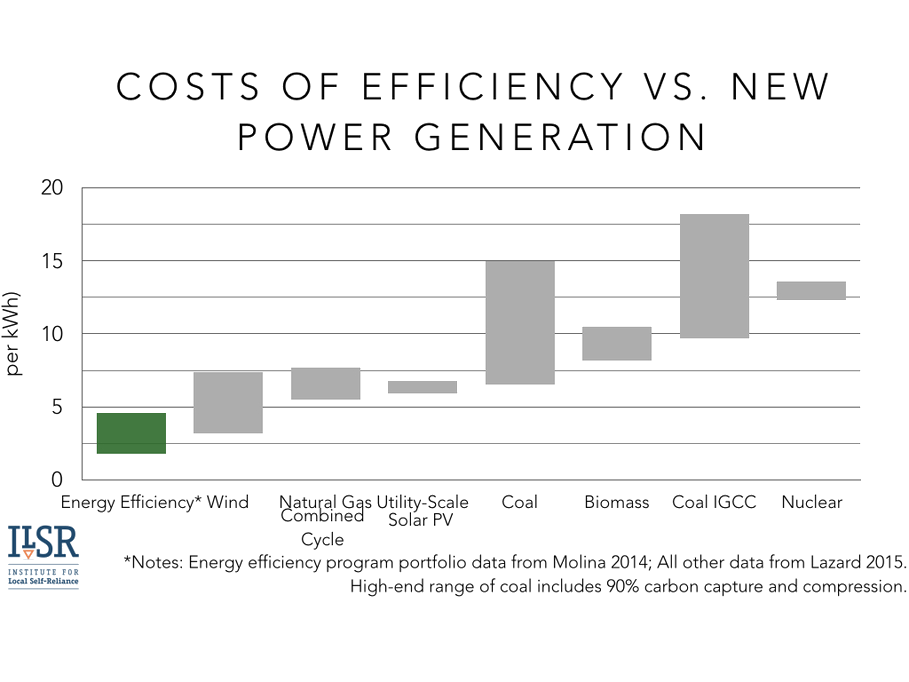

From smartphones to solar, the onslaught of new technology has reconfigured how Americans view energy use and consumption. It’s also flipped the calculus of utility companies in meeting energy supply. The crux of this new paradigm is that the cheapest new energy supply is energy saved through conservation and efficiency, not expensive new generation. The following chart illustrates the cost of procuring new kilowatt-hours of electricity from energy efficiency compared to new power plants.

The economics of energy efficiency and renewables permeate the marketplace. For every $1 invested in efficiency, utility customers see between $1.24 and $4.00 in benefits, including smaller bills and avoided expenses tied to building new infrastructure. That frees up substantial savings that can be spent elsewhere, stimulating the local economy.

There’s also ample evidence that distributed solar provides more value to the grid that its producers receive in compensation. Minnesota’s “value of solar” formula, for example, has consistently offered a higher price for solar — based on its value to the grid and society — than producers receive if they simply received bill credits based on the electricity produced.

Utilities can and must embrace a new way of doing business that favors energy efficiency and renewables, starting with a tool that enables all customers to choose lower energy costs.

[RETURN TO TOP]

A Powerful, Universal Tool: Inclusive Financing

Since debuting more than a decade ago, an inclusive financing strategy — using tariffed on-bill investment programs — is steadily taking hold in multiple states around the country. Since on-bill programming in New Hampshire won regulatory approval in 2002, programs in Kansas, Kentucky, Arkansas, California, and North Carolina have followed. Other states and utilities are exploring such initiatives.

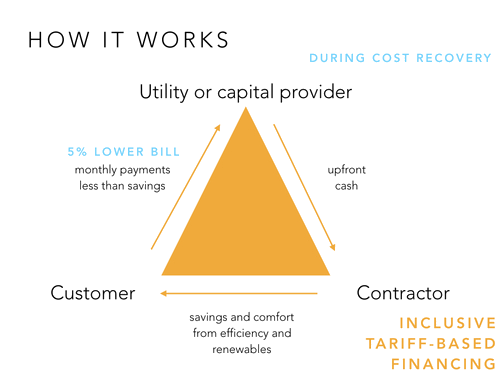

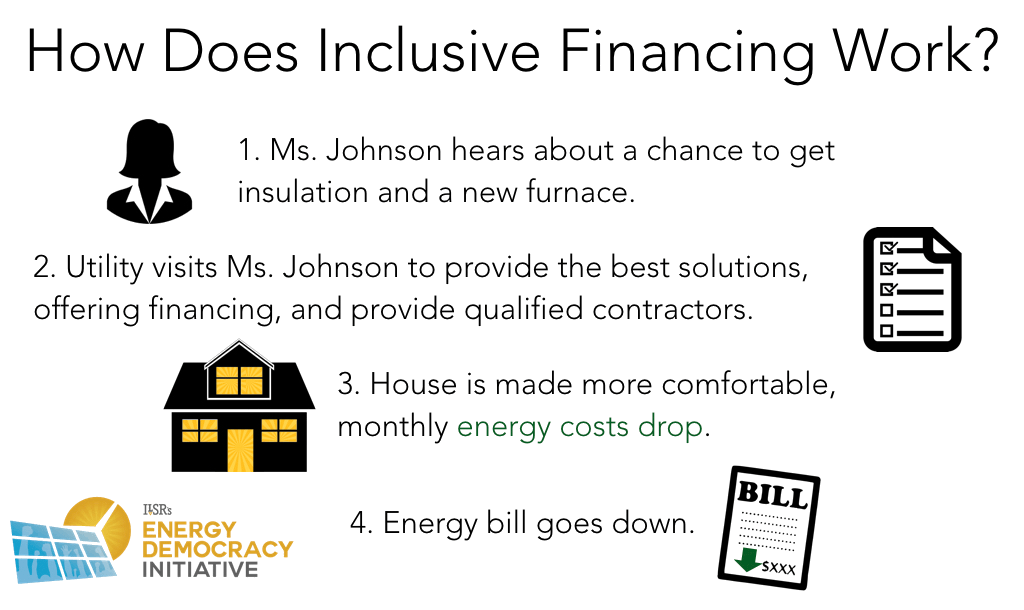

The program requires either the utility or a private investor to cover the upfront costs of qualifying energy improvements to homes or buildings. The utility recovers the costs on utility bills for the location, at a rate that is less than the estimated savings these improvements will produce. Charges that recover the cost of the upgrades over time appear as a line-item on customers’ monthly bills, simplifying the cost recovery process and increasing transparency.

Well-designed tariffs set up a system where whoever pays for the utility bill at a home or building also pays for — and directly benefits from — the more efficient home or rental unit.

Under the terms of this opt-in tariff, customers carry no lien or debt associated with their improvements. Assuming no other changes in energy consumption habits, they get immediate net savings on their electric and/or gas bills, plus a more comfortable and sustainable home. If the upgrade (like a new furnace) fails and is not repaired, they don’t make payments until it is repaired.

Roanoke Electric, based in North Carolina, runs one of the existing programs. It initially sought to cut customers’ energy costs with improvements financed using loans, but that model required customers — many with low incomes and shut out of traditional financing — to receive loan approval and take on debt. Roanoke contacted 1,000 of its customers about the program, and more than 100 signed up, but fewer than 10 were ultimately able or willing to secure the loan.

The utility has since implemented a tariffed on-bill investment program based on the Pay As You Save® (PAYS®) framework, which is demonstrably more effective and has served many of the customers unable to participate in its loan program. After changing the financing model, the utility reports, customer interest — and results — gained substantial momentum.

Program Design

The capital for energy-saving or energy-generating improvements can come from the utility itself or from a third party. In general, utilities can source capital for making loans or tariffed investments from private capital markets or public financing facilities.

Stitching tariffs into energy efficiency programs was a relatively novel idea in 2002 when New Hampshire introduced a pilot initiative that seeded permanent on-bill programming. After years of refinement and field data, the framework was recognized in a 2014 report as a potential “game-changer” because of its potential to deliver robust security and overcome a range of barriers to efficiency beyond upfront costs. Renters can participate, municipalities can participate without a public vote, and customers can participate without taking on new debt. Also, tariffed on-bill programs remove barriers for customers unable to risk that upgrades could fail (and stop producing savings) during the cost recovery period. They also address barriers for customers that cannot bear the risk of higher near-term costs in exchange for long-term savings because they lack the extra income.

Of the 30 on-bill programs examined in the 2014 report, 10 offered line-item billing and 13 offered on-bill loans, while just seven leveraged on-bill tariffs (and confusingly, some of those still use loan financing). For a breakdown of information on those programs, see the appendix to the Financing Energy Improvements on Utility Bills from SEEAction.

Investor-owned, cooperative, and municipal utilities can all implement inclusive financing for energy-saving improvements. Each of these types of utilities is represented among the seventeen utilities that have or are offering programs in seven states. With a tariff on-bill investment program, the utility owns the improvements until it recovers the cost through a site-specific charge on the bill, then the building owner takes ownership at no additional cost. Because tariff ties the investment to the meter and not an individual customer, the payments and upgrades apply to both the current and successor occupants of a given property until the utility’s costs are recovered.

Tariffed on-bill programs remove barriers for customers unable to risk that upgrades could fail (and stop producing savings) during the cost recovery period. They also address barriers for customers that cannot bear the risk of higher near-term costs in exchange for long-term savings they lack the extra income.

As a condition of participation, utilities can require customers to keep the upgrades operational. Those pursuing more efficient air conditioning systems, for example, are responsible for changing filters. Some utilities offer a service agreement that can be included with the upgrades so that annual maintenance for HVAC systems is assured.

The terms of the tariff can also address the potential for equipment breakdown during the period of cost recovery. If new energy-efficient equipment stops working or underperforms, the customer can notify the utility or its program operator, which suspends charges for cost recovery until the utility — likely through the contracted installer — determines why it failed and a plan to fix it. This provision in the tariff protects customers, and the risk for utilities is also low when eligible improvements include proven technologies installed by certified contractors.

Key Results

There are a range of options for implementing tariffed on-bill programs. Not all of them improve access for traditionally under-served customers. If properly designed, however, tariffed on-bill programs can deliver immediate cost savings, allow near-universal participation, remove financial and non-financial barriers, and provide deeper energy and cost savings than traditional energy savings programs.

The following chart illustrates several of these benefits, comparing inclusive financing via tariffed on-bill programs to traditional consumer-loan-based financing for energy efficiency.

Immediate Savings

Tariffed on-bill programs can deliver immediate financial benefits to customers by supporting cost-effective energy improvements and by structuring the cost recovery to reflect the life of upgrades. In the following graphic, for example, the customer’s energy bill initially falls by 5% — the net effect of the energy savings exceeding the cost recovery charge. After the utility recovers its costs, however, the customer enjoys the full energy savings, which can rise to 25% or higher.

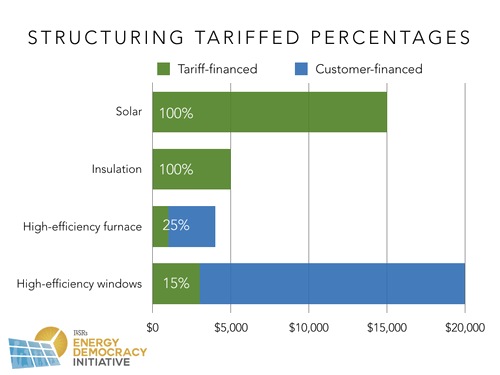

Choosing cost-effective measures is a balance of customer interest and utility knowledge. Midwest Energy, a cooperative serving Kansas member-owners, helps finance the full cost of projects that yield significant savings, but only part of the cost of projects (such as new windows) that have a lesser impact on energy use. The following chart illustrates in generic terms how a program might be structured for a variety of measures. A tariffed on-bill program can finance any on-site upgrades estimated to generate sufficient energy savings to cover the cost recovery charge and produce net savings.

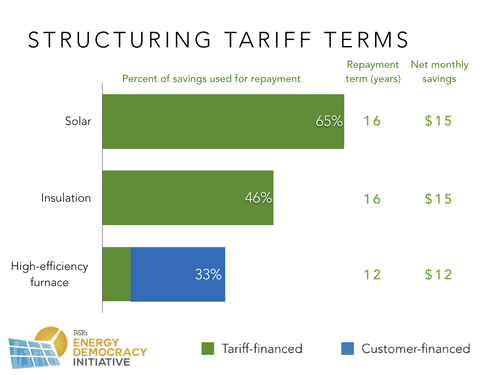

Setting the period of cost recovery is also important, both to ensure that the upgrades will continue to perform for a period that is longer than the cost recovery charges apply, and also to reduce monthly payments. Program operators for tariffed on-bill programs can calculate cost recovery plans that allow customers to generate savings even as the utility recovers its costs for the energy upgrades. As a general rule under the Pay As You Save® (PAYS®) system, programs are designed to recover costs for measures within 80% of their useful life, and to use no more than 80% of the estimated average bill savings for cost recovery.

The following chart illustrates cost recovery terms for three common items: solar PV, insulation, and a new furnace. The data is based on a cost of capital of 3% for tariffed investments, with cost recovery extending to 80% of the useful life of the upgrades, and the estimated average monthly savings exceeding average monthly cost recovery charges.

Tariffed on-bill programs that don’t provide financing terms that deliver immediate savings expose future residents to the risk of paying more than they save. Assuring that a portion of the estimated average savings stay with the customer from the start has been essential to win support for a tariffed on-bill programs.

Universal Access

By using a utility tariff rather than a loan as the financing mechanism, tariffed on-bill programs can avoid the hazards of other energy savings programs that restrict access to those with prime credit scores or who own their buildings. Credit-based programs, often paired with utility rebates, lock out less-affluent customers, leaving them to effectively subsidize wealthier customers’ use of the incentives. This is particularly true for renters, who are chronically underrepresented in the population of participants in utility energy efficiency programs for which funds are drawn from all customers.

A tariff-based program, on the other hand, uses a time-tested method of applying charges to a customer’s utility bill to recover costs for system improvements. Utilities have many tariffs for different classes of customers, and they have tariff riders such as charges for fuel costs, environmental compliance, or transmission lines. An opt-in tariff for energy efficiency upgrades differs by being voluntary for customers with cost effective investment opportunities at their location.

Although a tariff is more straightforward, an on-bill loan program in South Carolina (and soon in Holland, MI) called Help My House captures some of the key elements of a tariff-based program. The estimated savings need to exceed costs, and the loans may be transferable to the new owner if the state adopts a law that makes it legal to do so. Laws in both states direct loan programs to be structured in this way. |

There are several advantages to a tariff-based program. First, the utility ties cost recovery for its investment to its meter at that location and not the person. This allows customers to make investments that may outlive their residency at the property, with the confidence that they won’t be stuck with the tab if they move.

Additionally, the energy savings from high-efficiency furnaces or production from rooftop solar provide more energy resources that help meet the system requirements for the utility — relaxing the pressure to build more supply infrastructure like power plants and pipelines that they also finance using tariffs. A tariff is a tool for financing distributed energy solutions, and applying that tool to let customers develop on-site energy resources makes sense if those energy resources provide the system with valuable benefits (for more on the “value of solar,” for example, see ILSR’s 2014 report).

The energy savings from high-efficiency furnaces or production from rooftop solar provide more energy resources that help meet the system requirements for the utility – relaxing the pressure to build more supply infrastructure such as power plants and pipelines financed using tariffs.

The tariff-based model lets customers participate who would otherwise be unlikely to have access to financing for energy improvements, including those with subprime credit or low incomes.

Tariffed on-bill programs can also improve energy savings options for renters by allowing tenants (who pay their utilities directly) to access financing, or by helping rental property owners that do pay for energy service the same access to tariffed on-bill investments. That’s especially important in urban areas with a high proportion of rental properties — nearly 40% on average — and for renters who typically have little incentive to invest in energy savings measures in a property they do not own.

In Minneapolis, for example, owner-occupied homes comprised just 48.6 percent of the housing stock between 2010 and 2014, according to the most recent Census data available. That means most housing units are rentals, virtually untouchable under less progressive on-bill repayment policy. Plus, the city is adding rental units to the mix – it permitted 141 in July 2016 alone, continuing steady expansion.

Simplicity

Tariffed on-bill programs provide a simpler path to energy efficiency and renewables, like rooftop solar, rather than forcing customers to navigate the complicated process of finding financing on their own. Better tariffed on-bill programs incorporate efficiency and renewable energy assessments and contractor recommendations to help customers discover and vet their options.

Bigger Savings

Tariffed on-bill programs are useful for customers considering a wide range of cost-effective improvements in both the residential and commercial market segments, including municipal buildings like schools and city facilities. Research by Clean Energy Works shows customers offered tariffed on-bill investment programs instead of a consumer loan tend to invest twice as much in energy improvements. The reason for this increased willingness to accept larger projects with deeper savings is that program participants face fewer risks. They receive immediate net savings and have no obligation to pay for the upgrades if they move away. Also, if the upgrades fail to function, the charges are suspended until the utility or its program operator arranges a repair or remedy.

These conditions allow a customer to manage their risk and assures them access to support if the equipment installed does not function. As a result, at every utility offering a tariffed on-bill program, more than half of all customers receiving an offer to install energy saving improvements accept them, and when they accept, the size of the average project tends to be twice as large as reported for on-bill loan programs.

High Cost Recovery Rate

A synthesis of various on-bill programs in place throughout the U.S. showed a default rate below 1 percent — far below the prevailing national consumer loan default rate (3.28% from 1991-2016). In other words, utilities or their capital providers face minimal risk of non-payment when seeking to recover costs for cost effective energy upgrades.

Typical consumer loan underwriting standards tend to refer to indicators that would overestimate the likelihood that a customer will not make payments due for energy-saving investments. Unlike car loans, for example, tariffed on-bill investments in energy efficiency or solar make money for the customer. A credit score estimates the likelihood of paying back borrowed money in general, not the likelihood of continuing to pay a utility bill after it shrinks. Therefore, on-bill loan programs tend to disqualify prospective participants based on an assessment of creditworthiness that is not consistent with the observed non-payment rate of less than 1%.

Unlike car loans, for example, tariffed on-bill investments in

energy efficiency or solar make money for the customer.

Midwest Energy in Kansas, which has one of the most established tariffed on-bill programs, has vetted gas and electric efficiency upgrades for 2,500 properties. More than half of those customers opted into the program, pushing the total value of improvements past $8 million. Despite the expansiveness of the program, the utility’s cost recovery rate is above 99.9 percent.

[RETURN TO TOP]

A Time-Tested Tool

Tariff-based on-bill repayment allows utilities to tap into a familiar method to expand investment in upgrades that curb energy use and customer costs. The tariff structure represents an agreement with customers to recover costs initially paid by a utility. Historically, energy providers have used tariffs to pay for new power plants, power lines, or pipelines.

In tariffed on-bill programs targeting customer-sited energy efficiency and renewables, a tariff functions similarly by providing the utility with benefits such as energy efficiency as an energy source in exchange for the upfront capital. It differs in that cost recovery is achieved through charges only to the upgraded site rather than a specific class of customers. Because energy efficiency tends to be the lowest-cost energy resource, and because on-site energy generation has such high value, benefits achieved by a utility’s investment these type of cost effective energy upgrades to homes or businesses, public facilities, or institutions can also deliver benefits to all the utility’s customers, such as lower wholesale operating costs and relaxed pressure to build more infrastructure to meet peak demand.

Historically, energy providers have used tariffs to pay for new power plants, power lines, or pipelines.

In tariffed on-bill programs targeting customer-sited energy efficiency and renewables, a tariff functions similarly by providing the utility with benefits such as energy efficiency as an energy source in exchange for the upfront capital.

Put simply, tariffed on-bill programs allow utilities to make investments in energy efficiency and renewable energy upgrades at specific sites, resulting in system-wide benefits. Utilities recover the cost of those investments from the customers at the sites where the upgrades are installed. The utility cashes in on lower costs to meet customer demand, while the customer reduces their energy costs.

Inclusive Financing in Practice

Roanoke Electric Cooperative

North Carolina-based Roanoke Electric has a high-performing tariffed on-bill program, which is operated by a non-profit associated with the utility. To date, the program has tackled upgrades in 120 of its members’ homes and the utility reports an average cost of $6,900.

The estimated average monthly net savings for participating customers in that initial group is $58 as they pay the monthly repayment charge, with estimated average monthly gross savings of about $120. That translates to $1,440 per year in total savings and an annual net financial impact of almost $700, a substantial gain especially for those in lower income brackets.

Program benefits extend to the utility itself. Roanoke Electric reports paying a lower demand charge for the supply of power it purchases, thanks to greater efficiency among its customers. By all metrics, the utility says the program has beat its expectations — especially notable after its initial loan-based program got off to a disappointing start when very few customers were able or willing to take on debt.

Ouachita Electric Cooperative

After implementing a tariff-based on-bill program, Ouachita Electric saw a surge of interest from its customer base in south Arkansas. In the first three months, the number of customers seeking efficiency assessments — a precursor to improvements — doubled from 73 to more than 162.

As of August, 100% of multifamily and rental units that received an offer of investment through the program have opted in. Meanwhile, 92% of single-family customers that received offers to invest in upgrades at their residence signed on. The program provides a much-needed pathway to energy efficiency and savings in a persistent poverty area. Without it, many customers, unable to cover the upgrade costs themselves, pay $300 or more per month in some months to keep their lights on.

Using smart meters, Ouachita carefully tracks cost savings. It has determined that the program lowers its demand charges and will, in the long run, curtail the need to add expensive new generation capacity.

Conclusion

Inclusive financing offers proven benefits for both utilities and the communities they serve. Tariff-based on-bill programs in particular can bridge troubling gaps in today’s energy marketplace, bolstering energy efficiency and renewables for all customers.

Most utility programs fail to reach a majority of a utility’s customers: residential and commercial renters, those unable or unwilling to assume debt, those unable to assume the risk that upgrades may fail during cost recovery, and those unable to make payments upfront. This creates an especially untenable situation for low-income households facing the heftiest utility bills. Well-designed finance programs, accessible across the board, can address barriers that dampen participation, yielding a meaningful economic boost at the individual and community scale.

Tariffed on-bill financing is a natural step for utilities and customers committed to increasing energy efficiency and promoting renewables. The demonstrated success in markets across the U.S., especially those serving high concentrations of low-income customers, showcases its potential for meaningful economic impact.

[Return to top]

Sources

A Huge Opportunity

American Council for an Energy-Efficient Economy. “Next Generation Standards: How the National Energy Efficiency Standards Program Can Continue to Drive Energy, Economic, and Environmental Benefits.” August 2016. https://aceee.org/sites/default/files/publications/researchreports/a1604.pdf.

UtilityDive. “Why utilities could soon face massive load defection, and how they can prevent it.” April 2015. https://www.utilitydive.com/news/why-utilities-could-soon-face-massive-load-defection-and-how-they-can-prev/383558/

American Council for an Energy-Efficient Economy. “America’s Abundant, Untapped Energy Efficiency Resource.” March 2011. https://aceee.org/files/pdf/fact-sheet/Basic%20EE%20Fact%20Sheet.pdf

EnergySage. “Solar Panels in Minnesota.” Accessed August 2016. https://www.energysage.com/solar-panels/mn/

American Council for an Energy-Efficient Economy. “How Does Energy Efficiency Create Jobs?” November 2011. https://aceee.org/files/pdf/fact-sheet/ee-job-creation.pdf

The Solar Foundation. “National Solar Jobs Census 2015.” January 2016. https://www.thesolarfoundation.org/wp-content/uploads/2016/01/TSF-2015-National-Solar-Jobs-Census.pdf

Institute for Local Self-Reliance. “Citizens give ‘going Boulder’ a new meaning: local energy self-reliance.” November 2011. https://ilsr.org/citizens-give-going-boulder-new-meaning-local-energy-self-reliance/

Institute for Local Self-Reliance. “The History and Hope for a First-in-the-Nation City-Utility Clean Energy Partnership.” November 2014. https://ilsr.org/history-hope-first-in-the-nation-city-utility-clean-energy-partnership/

Challenges to Reaching Most Customers

Rappahannock Electric Cooperative. “Saving Energy Saves Money.” https://www.myrec.coop/content-images/A-881.jpg

{kind=link}

Opower and American Council for an Energy-Efficient Economy. “Myths of Low-Income Energy Efficiency Programs: Implications for Outreach.” 2014. https://aceee.org/files/proceedings/2014/data/papers/7-287.pdf

Evaluation + Strategy for Social Innovation, American Council for an Energy-Efficient Economy. “Who’s Participating and Who’s Not: The Unintended Consequences of Untargeted Programs.” June 2016. https://docketpublic.energy.ca.gov/PublicDocuments/16-OIR-02/TN211734_20160607T141453_Who%27s_Participating_and_Who%27s_Not_the_unintended_consequences_o.pdf

American Council for an Energy-Efficient Economy. “Lifting the High Energy Burden in America’s Largest Cities: How Energy Efficiency Can Improve Low-Income and Underserved Communities.” April 2016. https://aceee.org/research-report/u1602

Inside Energy. “High Utility Costs Force Hard Decisions For The Poor.” May 2016. https://insideenergy.org/2016/05/08/high-utility-costs-force-hard-decisions-for-the-poor/

Fisher Sheehan and Colton. “Home Energy Affordability Gap.” Accessed August 2016. https://www.homeenergyaffordabilitygap.com/01_whatIsHEAG2.html

Marte, Jonnelle. “The majority of consumers have subprime credit scores, report says.” Washington Post, 1/29/15. Accessed December 2016. https://wapo.st/2gZm0Jh

“Quarterly Vacancy and Homeownership Rates by State and MSA.” U.S. Census Bureau. Accessed December 2016. https://www.census.gov/housing/hvs/data/rates.html

A Necessary Paradigm Shift

American Council for an Energy-Efficient Economy. “The Best Value for America’s Energy Dollar: A National Review of the Cost of Utility Energy Efficiency Programs.” March 2014. https://aceee.org/research-report/u1402

A Powerful, Universal Tool: Inclusive Financing

Local Clean Energy Alliance. “State On-Bill Financing and PAYS Programs.” 2014. https://www.localcleanenergy.org/State%20On-Bill%20Financing

New Hampshire Electric Co-op. “SmartSTART.” https://www.nhec.com/business_energysolutions_smartstart.php

Institute for Local Self-Reliance. “A Kansas Electric Cooperative Offers Energy Savings with $0 Down — Episode 32 of Local Energy Rules Podcast.” April 2016. https://ilsr.org/a-kansas-electric-cooperative-offers-energy-savings-with-0-down-episode-32-of-local-energy-rules/

MACED. “How$martKY Overview.” 2015. https://www.maced.org/howsmart-overview.htm

Ouachita Electric Cooperative, EEtility, and Clean Energy Works. “Opening Opportunities with Inclusive Financing for Energy Efficiency: Preliminary Results of the Ouachita Electric HELP PAYS Program.” November 2016. https://www.oecc.com/pdfs/Ouachita%20Electric%20HELP%20PAYS%20Program%20-%20First%204%20Months%20of%20Activity-1.pdf

Local Clean Energy Alliance. “California On-Bill Financing Programs.” 2014. https://www.localcleanenergy.org/California%20On-Bill%20Financing%20Programs

Roanoke Electric Cooperative. “Sharing Insights of Our Experience with Pay As You Save (PAYS).” 2015. https://www.roanokeelectric.com/content/PAYS

UtilityDive. “On-bill financing a popular option for Midwest utilities’ efficiency upgrades.” November 2015. https://www.utilitydive.com/news/on-bill-financing-a-popular-option-for-midwest-utilities-efficiency-upgrad/408480/

Program Design

New Hampshire Public Utilities Commission. “PAYS: Preliminary Results of New Hampshire Pilots.” June 2003. https://aceee.org/files/pdf/conferences/eer/2003/Brockway-5w.pdf

State and Local Energy Efficiency Action Network. “Financing Energy Improvements on Utility Bills: Market Updates and Key Program Design Considerations for Policymakers and Administrators.” May 2014. https://www4.eere.energy.gov/seeaction/sites/default/files/pdfs/onbill_financing.pdf

State and Local Energy Efficiency Action Network. “Financing Energy Improvements on Utility Bills: Technical Appendix — Case Studies.” May 2014. https://www4.eere.energy.gov/seeaction/system/files/documents/publications/chapters/onbill_financing_appendix.pdf

State and Local Energy Efficiency Action Network. “Financing Energy Improvements on Utility Bills: Market Updates and Key Program Design Considerations for Policymakers and Administrators, Technical Appendix: Case Studies.” May 2014. https://www4.eere.energy.gov/seeaction/sites/default/files/pdfs/onbill_financing.pdf

Immediate Savings

Institute for Local Self-Reliance. “A Kansas Electric Cooperative Offers Energy Savings with $0 Down.” April 2016. https://ilsr.org/a-kansas-electric-cooperative-offers-energy-savings-with-0-down-episode-32-of-local-energy-rules/

Universal Access

Institute for Local Self-Reliance. “Minnesota’s Value of Solar Can a Northern State’s New Solar Policy Defuse Distributed Generation Battles?” April 2014. https://ilsr.org/wp-content/uploads/2014/04/MN-Value-of-Solar-from-ILSR.pdf

United States Census Bureau. “QuickFacts: Minneapolis, Minnesota.” July 2015. https://www.census.gov/quickfacts/table/HSG010215/2743000,27

Star Tribune. “New home construction permits rose slightly in Twin Cities this month.” July 2016. https://www.startribune.com/new-home-construction-permits-rose-slightly-in-twin-cities-this-month/388665481/

High Cost Recovery Rate

State and Local Energy Efficiency Action Network. “Financing Energy Improvements on Utility Bills: Market Updates and Key Program Design Considerations for Policymakers and Administrators, Technical Appendix: Case Studies.” May 2014. https://www4.eere.energy.gov/seeaction/sites/default/files/pdfs/onbill_financing.pdf

Board of Governors of the Federal Reserve System. “Charge-Off and Delinquency Rates on Loans and Leases at Commercial Banks.” 2016. https://www.federalreserve.gov/releases/chargeoff/delallsa.htm

Clean Energy Solutions Center. “Inclusive Financing for Distributed Energy Solutions.” May 2016. https://cleanenergysolutions.org/sites/default/files/documents/2015-05-26-transcript.pdf

A Time-Tested Tool

American Council for an Energy-Efficient Economy. “On-Bill Financing for Energy Efficiency Improvements.” April 2012. https://aceee.org/files/pdf/toolkit/OBF_toolkit.pdf

Institute for Local Self-Reliance. “Utility Solar May Cost Less, But It’s Also Worth Less.” July 2015. https://ilsr.org/utility-solar-may-cost-less-but-its-also-worth-less/

Inclusive Financing in Practice

Roanoke Electric Cooperative

Clean Energy Solutions Center. “Inclusive Financing for Distributed Energy Solutions.” May 2016. https://cleanenergysolutions.org/sites/default/files/documents/2015-05-26-transcript.pdf

Ouachita Electric Cooperative

Clean Energy Solutions Center. “Inclusive Financing for Distributed Energy Solutions.” May 2016. https://cleanenergysolutions.org/sites/default/files/documents/2015-05-26-transcript.pdf

Ouachita Electric Cooperative, EETility, Clean Energy Works. “Performance of Inclusive Financing for Energy Efficiency: Preliminary Results of the Ouachita Electric HELP PAYS Program.” October 2016. https://www.oecc.com/pdfs/Ouachita%20Electric%20HELP%20PAYS%20Program%20-%20First%204%20Months%20of%20Activity%20-%20Posted%20Oct%2012%202016.pdf

Photo Credit: Chris Potter via Flickr (CC 2.0)

![]()

![]()

![]()

![]()