Our team fights the unchecked power of corporate monopolies and champions policies that level the playing field for small independent businesses.

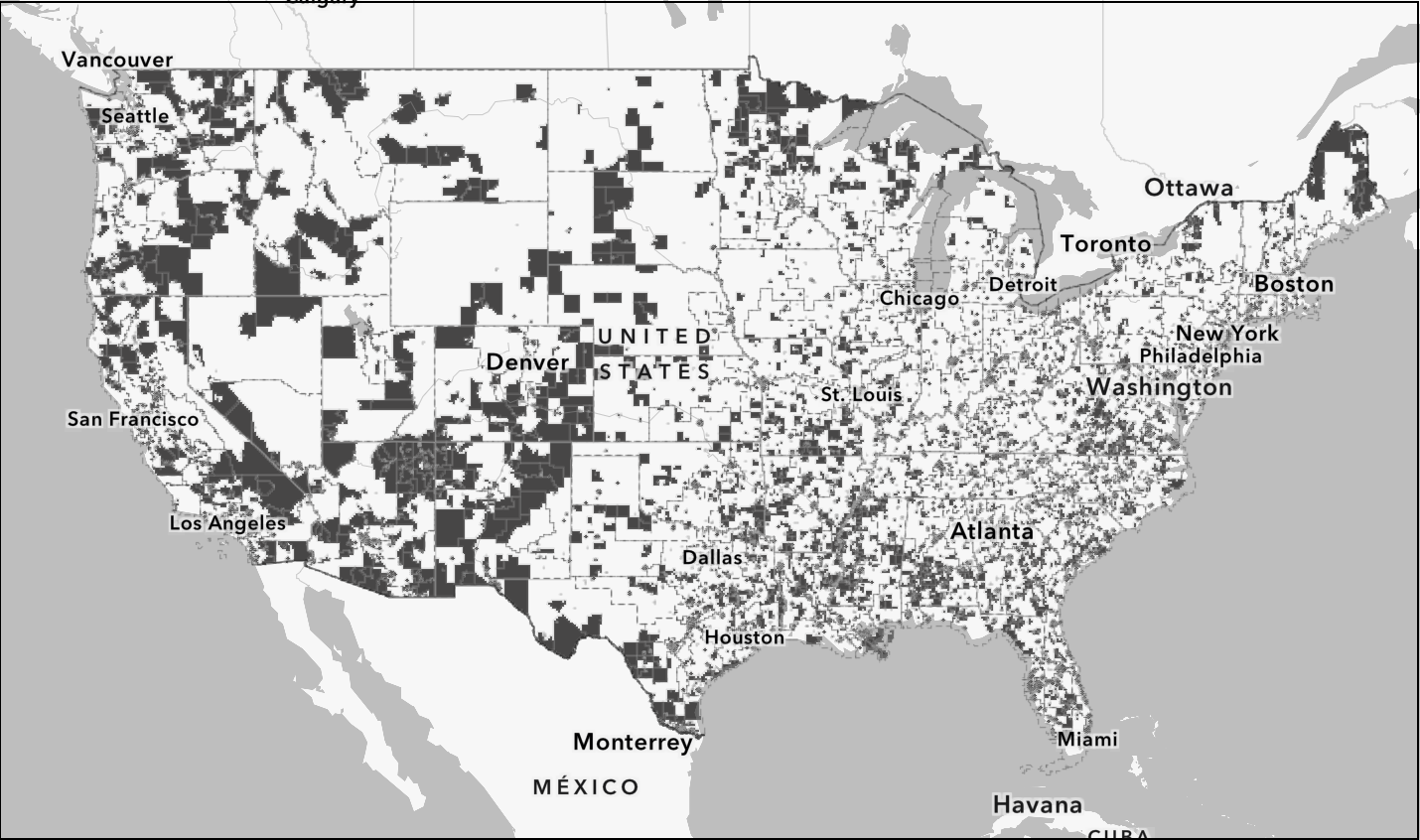

Mapping Food Deserts and Grocery Consolidation

To illuminate how consolidation shapes food access, ILSR created an interactive map that shows food deserts alongside the location of different types of grocery stores — independent, small chains, large chains, and megachains like Walmart and Kroger.

In The Sling: Live Nation and the Return of State Enforcement

Ron Knox reflects on the importance of state antitrust enforcement, both historically and today, and why it matters for more than just the Ticketmaster case.

In The Forge: ILSR Superteam Talks Local Power and Fighting Corporate Control

Three ILSR staffers talked to Liberation in a Generation and The Forge about the many dimensions of fighting corporate power — and building local power.

In Washington Monthly: Amazon’s AI Algorithms are Raising Prices

Online price swings may look like fierce competition. In reality, they’re part of an invisible strategy Amazon uses to maintain its dominance of e-commerce and...

Amazon's stranglehold crushes small businesses and stifles innovation. We’re laying the groundwork to break up the tech giant and rebuild community-powered economies.

We expose how big chains use price discrimination to drive out local grocers and create food deserts — and we advance solutions that restore fair competition.

States have the power to pass and enforce laws that rein in corporate concentration. We track how states are using their authority and advocate for more action.

Our Small Business Rising coalition unites over 250,000 independent businesses nationwide to demand stronger antitrust laws, break up monopolies, and create a level playing field.

We equip citizens with local, state, and federal strategies and practical tools to grow local businesses — from zoning reforms to procurement policies to local development initiatives.

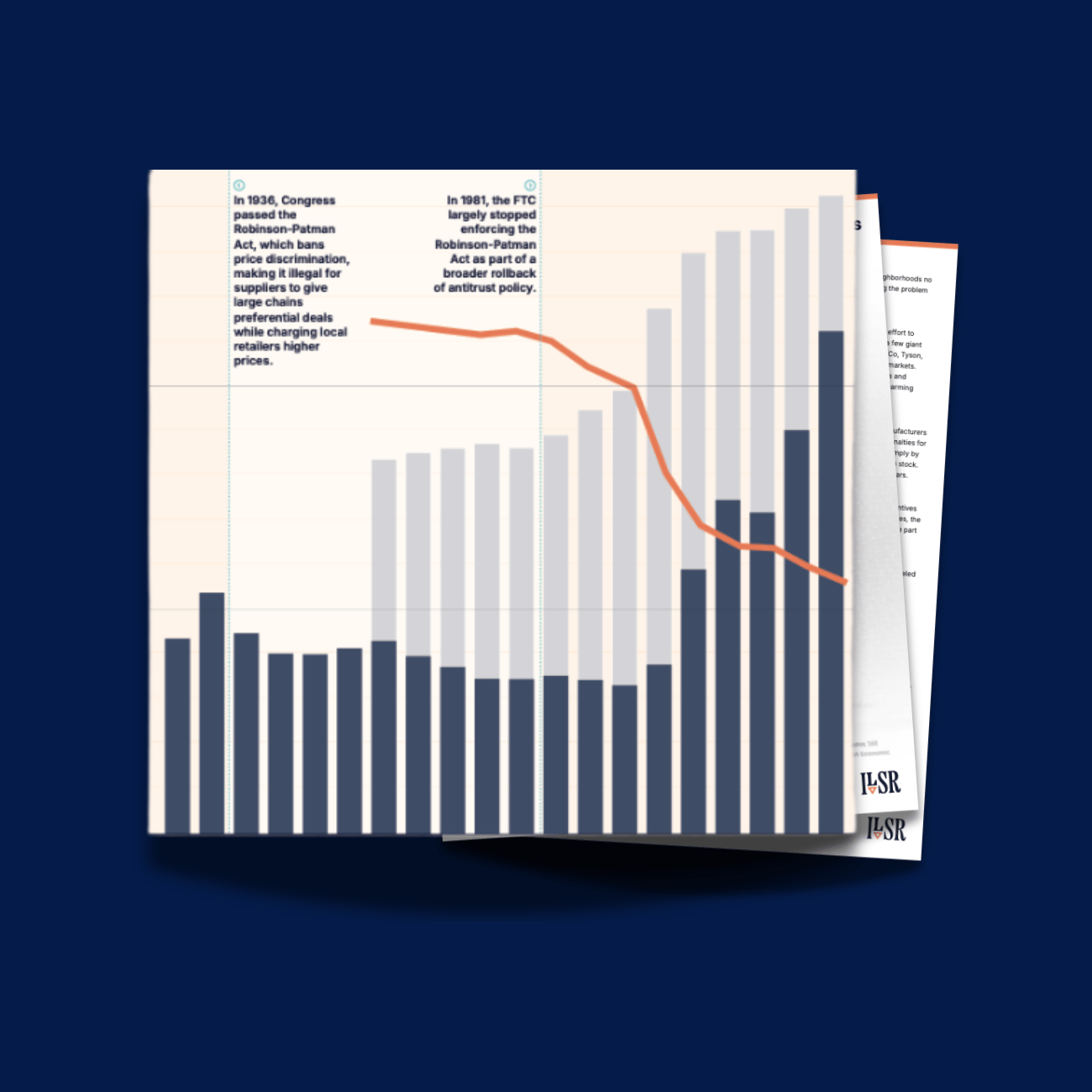

The Policy Shift That Decimated Local Grocery Stores

New data from ILSR highlights the direct link between the decline in Robinson-Patman enforcement and the collapse of independent grocers — a clear example of how policy decisions shape our communities and everyday lives.

Stacy Mitchell explains why this pivotal moment in antitrust can last beyond its current leaders at our enforcement agencies. Her piece is part of a...