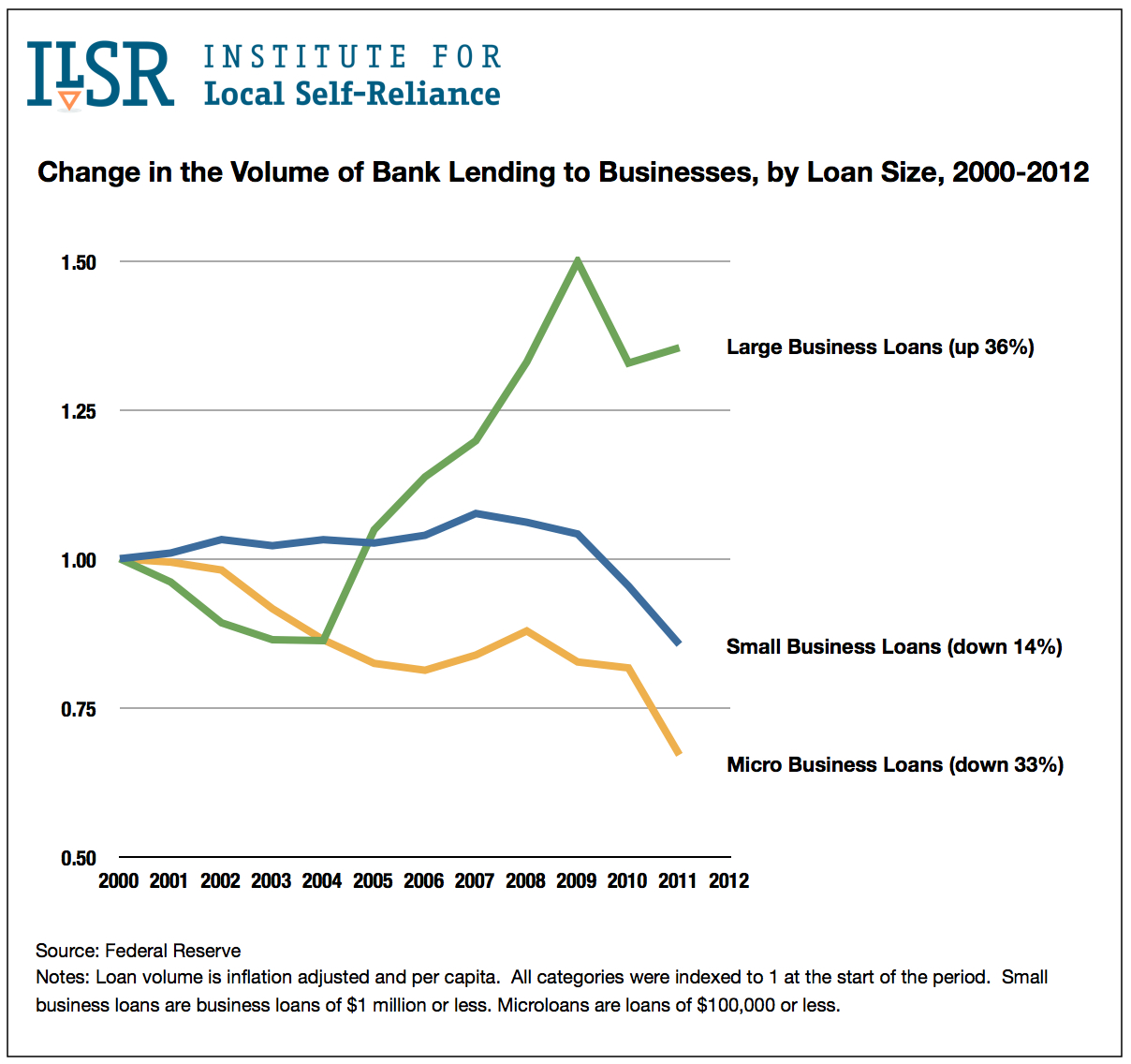

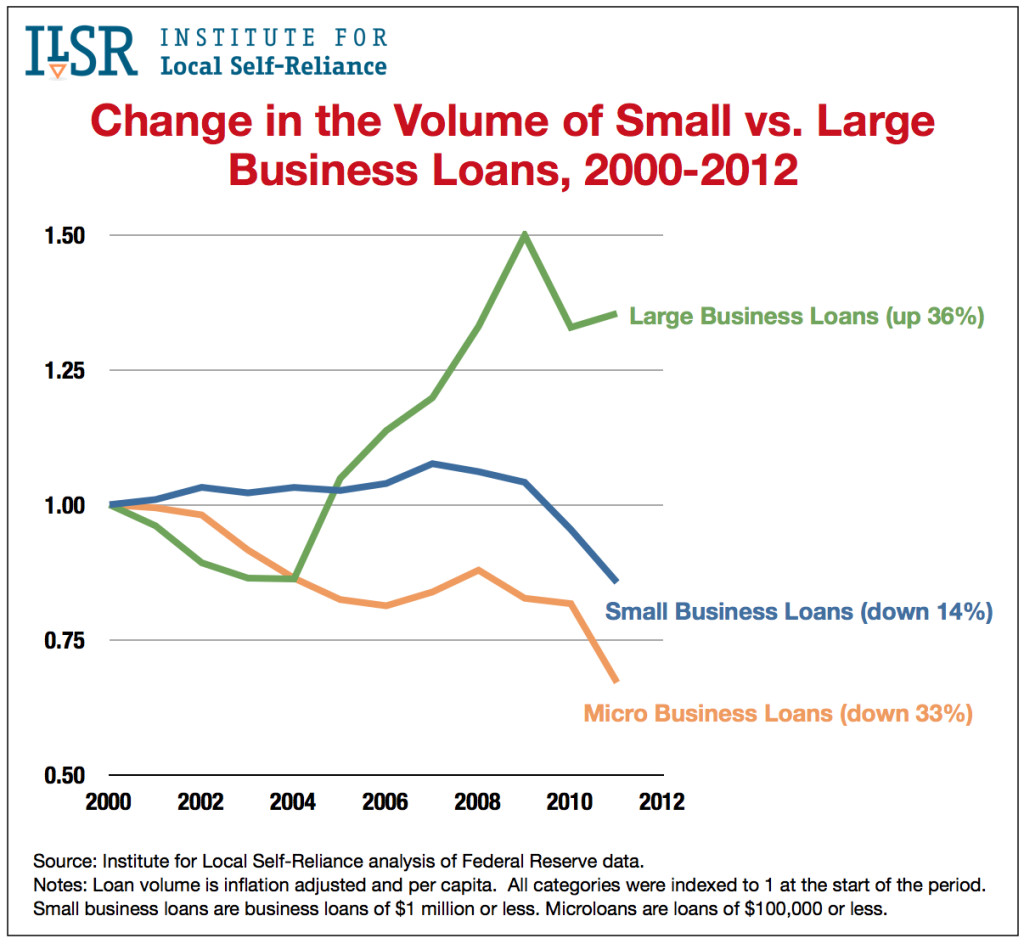

Even as their big competitors are awash in capital, many locally owned businesses are struggling to secure the financing they need to grow. A new ILSR analysis has found that, since 2000, bank lending to large businesses is up 36 percent, while small business loan volume has fallen 14 percent and “micro” business loans — those under $100,000 — have plummeted 33 percent.

(The largest corporations do not even need to rely on bank loans, of course, but can finance their growth through the soaring stock and corporate bond markets.)

The problem is not a lack of demand. In our 2014 Independent Business Survey, 42 percent of business owners that needed a loan in the previous two years reported being unable to obtain one. Startups, businesses with fewer than 20 employees, and enterprises owned by minorities and women are having an especially difficult time. Even with the same business characteristics and credit profiles, small businesses owned by African-Americans and Latinos are less likely to be approved for loans, according to one recent study.

One consequence of this credit shortage is that many small businesses are either not adequately capitalized or have been forced to rely on high-cost alternatives, such as credit cards. Both scenarios make them more vulnerable to failing.

The broader consequences for our economy are significant. Studies show locally owned businesses are a primary source of net new job creation, contribute to higher median household incomes, and increase social capital. Yet independent businesses in many sectors are losing market share, while the number of new startups has steadily fallen over the last two decades. Insufficient capital is a key culprit driving these trends.

To shed light on this problem and help inform policy discussions, ILSR has published an overview of the small business lending landscape. Among the key takeaways:

- Local community banks provide a disproportionate share of small business loans. Indeed, it is their decline, in both numbers and market share, that is largely to blame for the constriction in small business lending. As local banks lose ground to big banks, there are fewer financial institutions focusing on small business lending and fewer resources devoted to it. The top 4 banks now control 43 percent of all banking assets, but account for only 16 percent of small business loans.

- Credit unions account for less than 7 percent of small business loans, but have significantly expanded their lending in the last decade, growing from $14 billion in business loans to over $44 billion today. Only about one-third of credit unions currently participate in this market, however.

- Federal loan guarantees, provided through the U.S.

Small Business Administration, have historically played an important role in expanding credit to small businesses that don’t quite meet conventional lending requirements. In an alarming trend, however, the SBA has dramatically reduced its support for smaller businesses and shifted more of its loan guarantees to larger businesses (which still count as “small” under the agency’s expansive definitions). Since the mid 2000s, the number of business loans under $150,000 guaranteed by the SBA each year has fallen from about 80,000 to 24,000. Meanwhile, the SBA’s average loan size has more than doubled to $362,000.

Small Business Administration, have historically played an important role in expanding credit to small businesses that don’t quite meet conventional lending requirements. In an alarming trend, however, the SBA has dramatically reduced its support for smaller businesses and shifted more of its loan guarantees to larger businesses (which still count as “small” under the agency’s expansive definitions). Since the mid 2000s, the number of business loans under $150,000 guaranteed by the SBA each year has fallen from about 80,000 to 24,000. Meanwhile, the SBA’s average loan size has more than doubled to $362,000. - Crowdfunding has garnered a lot of attention recently as a potential solution to the small business credit crunch, but crowdfunding remains a tiny drop in the bucket, compared to the resources of the banking system. At the beginning of 2014, banks and credit unions had about $630 billion in small business loans on their books. The total volume of business financing provided through crowdfunding amounts to less than one-fifth of 1 percent of this. Although crowdfunding will undoubtedly grow and could emerge as a valuable source of capital for local enterprises, it does not obviate the need to fix the structural problems in our banking system that are impeding the development of community-scaled enterprises.

ILSR’s overview outlines several policy approaches that focus on reducing concentration in the banking system, expanding community banks, allowing credit unions to make more loans to small businesses, and reorienting the SBA’s loan programs to once again meet the needs of truly small businesses.